The Week Ahead: April Jobs Report and AMD Earnings – What Investors Are Watching

TLDR

- The April jobs report drops Friday, with economists expecting around 60,000 jobs added

- Semiconductor earnings from AMD and Arm Holdings will test the AI trade thesis

- Consumer giants including Disney, McDonald’s, and Marriott report this week

- The S&P 500 and Nasdaq both closed at record highs on Friday

- AI spending by major tech firms has climbed to nearly $725 billion

The April jobs report and a wave of major earnings results will dominate market attention this week, giving investors fresh data on the health of the US economy.

The S&P 500 and Nasdaq Composite both closed at record highs on Friday. The S&P 500 gained just under 1% for the week, while the Nasdaq rose 1.1%. The Dow Jones fell 0.3% on Friday but still finished the week up 0.5%.

E-Mini S&P 500 Jun 26 (ES=F)

E-Mini S&P 500 Jun 26 (ES=F)

Last week was driven largely by Big Tech earnings. Five of the seven Magnificent 7 companies reported, and investors responded positively. Microsoft, Amazon, Meta, and Alphabet raised their combined AI spending plans from $670 billion to nearly $725 billion.

Analysts say the broader earnings picture is holding up too. Corporate profits continue to come in above expectations, and commentary from companies has been more positive than many expected given the current economic climate.

The Jobs Report Is the Week’s Biggest Event

Friday’s April jobs report is the headline economic event. Economists are forecasting around 60,000 jobs added, a sharp drop from the 178,000 added in March.

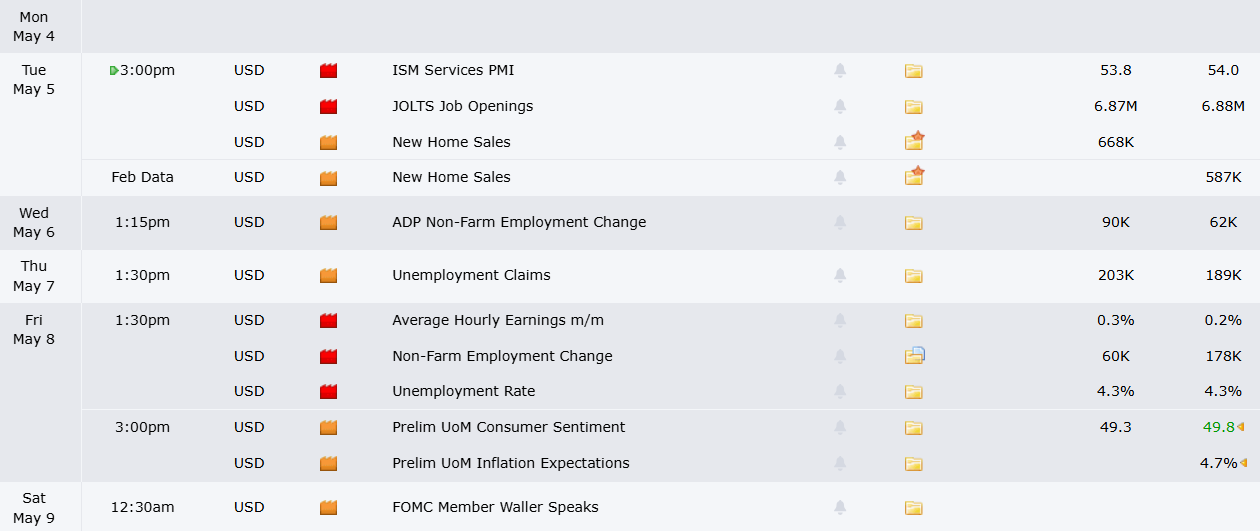

Source; Forex Factory

Source; Forex Factory

Initial jobless claims fell to their lowest level since 1969 last week, and private payroll data from ADP has shown signs of improvement. But the pattern of job gains and losses over the past 10 months has been uneven, making it hard to call a clear trend.

The Federal Reserve is watching closely. The central bank is weighing its next interest rate move as it monitors the labor market alongside energy prices tied to the ongoing conflict with Iran.

BNP Paribas economist Andrew Husby says AI-exposed sectors have seen slower hiring but not widespread job losses. He describes this as “growing the labor pie with AI,” suggesting technology is adding to economic output rather than simply replacing workers.

Before Friday, investors will also receive JOLTS job openings data on Tuesday, ADP private employment figures on Wednesday, and Challenger job cut data on Thursday.

Semiconductor Earnings Will Test the AI Trade

The semiconductor sector had its best month since February 2000 in April, with the PHLX Semiconductor Index surging more than 40%. Advanced Micro Devices is up 70% over the past month heading into its Tuesday earnings report. Arm Holdings is up 40%, and Lattice Semiconductor is up 25%.

Lattice Semiconductor reports Monday, Advanced Micro Devices on Tuesday, and Arm Holdings on Wednesday. These results will give investors a clearer picture of chip demand as AI infrastructure spending accelerates.

AMD recently announced plans to raise prices and struck a major deal with Meta. Analysts will be watching whether the company’s outlook matches the bullish signals from Big Tech’s spending plans.

Interactive Brokers strategist Steve Sosnick noted the sector’s gains make it vulnerable to a pullback, but added that continued positive earnings surprises would make it hard to bet against the sector.

Consumer Giants Report Across the Week

Away from tech and semiconductors, earnings from consumer-facing companies will offer a read on how Americans are spending.

Walt Disney reports Wednesday, with investors focused on streaming growth and theme park performance. Marriott reports Wednesday and Airbnb on Thursday, as the travel sector navigates higher airfares and fuel costs. United Airlines has said travel demand remains solid but expects pricing pressure in the second half of the year.

Fast food is also in focus. Restaurant Brands, parent of Burger King and Popeyes, reports Wednesday. McDonald’s reports Thursday and Wendy’s on Friday. Lower-income consumers have pulled back on fast food spending in recent months, and investors will be watching for any signs of improvement.

Palantir kicks off the week Monday after the close, followed by Novo Nordisk and Uber on Wednesday.

The post The Week Ahead: April Jobs Report and AMD Earnings – What Investors Are Watching appeared first on CoinCentral.

You May Also Like

Amkor Technology (AMKR) Stock Surges as Analyst Hikes Target to $90 Following Strong Q1 Results

Massive 331 Million USDT Transfer to Kraken Sparks Whale Alert and Market Speculation