Crypto’s killer app may be selling stocks after its own tokens failed retail

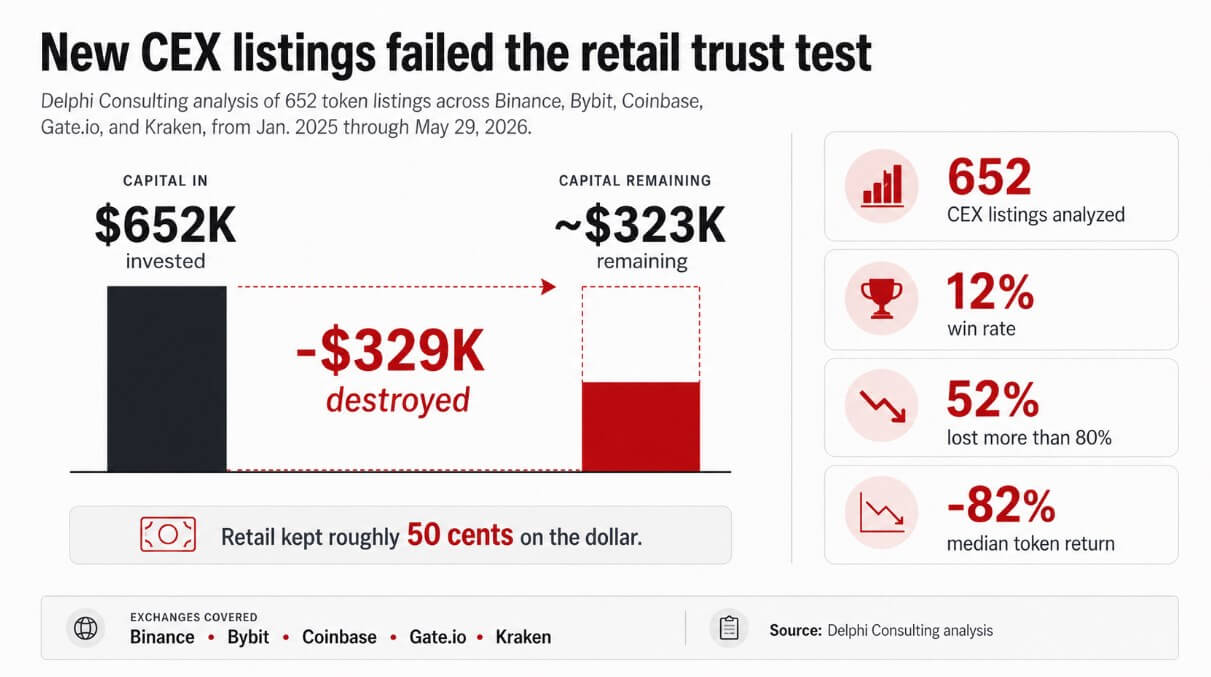

A Delphi Consulting analysis of 652 CEX listings from January 2025 onward found that a user buying every new token across Binance, Bybit, Coinbase, Gate.io, and Kraken would have kept roughly 50 cents on the dollar.

The win rate across all listings was 12%, 52% of tokens lost more than 80%, and the median return was -82%. Tokenized stocks appear to be the answer that exchanges are giving to failing token launches.

Delphi Consulting's analysis of 652 token listings across five major exchanges from January 2025 through May 2026 found a 12% win rate and a median return of -82%.

Delphi Consulting's analysis of 652 token listings across five major exchanges from January 2025 through May 2026 found a 12% win rate and a median return of -82%.

Kraken now offers more than 100 tokenized stocks and ETFs through its xStocks product, with 24/5 trading, $1 minimums, and self-custody support.

Robinhood EU lists more than 2,000 Stock Tokens linked to Nvidia, Microsoft, Apple, and the Vanguard S&P 500, with minimums of €1 and 24/5 access.

Coinbase offers stock and ETF trading inside the same app as crypto, with zero commission, USDC funding, and $1 fractional shares for US users, with a longer-term plan to make tokenized stocks available globally as on-chain collateral.

Tokenized stocks across all platforms held $1.48 billion in distributed value as of June 1, up 39% over 30 days, with $4.2 billion in monthly transfer volume.

What Binance Research says the opportunity is

Binance Research reported that equity ownership outside the US runs broadly below 20%, compared with 62% of Americans holding equities, attributing the gap to infrastructure access.

The same report projects that crypto exchanges could channel $2 trillion in incremental capital and nearly 300 million new users into global equity markets by 2031 under a base case, rising to $5 trillion in annual incremental equity capital under a bull case.

Some AI-cycle stocks traded above $1,000 per share during periods when average monthly wages in parts of Africa and Southern Asia were below $300, making single-share ownership inaccessible without fractional shares.

Binance says stablecoins could remove an average of 3.6% and about $40 per transaction in cross-border off-ramp costs, and that TradFi-linked perpetuals already account for roughly 10% of stablecoin trading volume, positioning stablecoins as general-market access infrastructure.

| Binance Research point | Why it matters for tokenized stocks |

|---|---|

| Equity ownership outside the US broadly below 20% vs 62% in the US | Large access gap for emerging-market users |

| Nearly 300M potential new users by 2031 | Crypto exchanges become global brokerage gateways |

| $2T base-case incremental capital by 2031 | Tokenized equities become a major financial access product |

| $5T bull-case annual incremental equity capital | Upside case if crypto rails become normalized equity infrastructure |

| Stablecoins can reduce off-ramp costs by 3.6% / ~$40 per transaction | Stablecoins become brokerage cash, not just crypto trading collateral |

| TradFi-linked perps at ~10% of stablecoin trading volume | Demand for non-crypto assets is already appearing inside crypto markets |

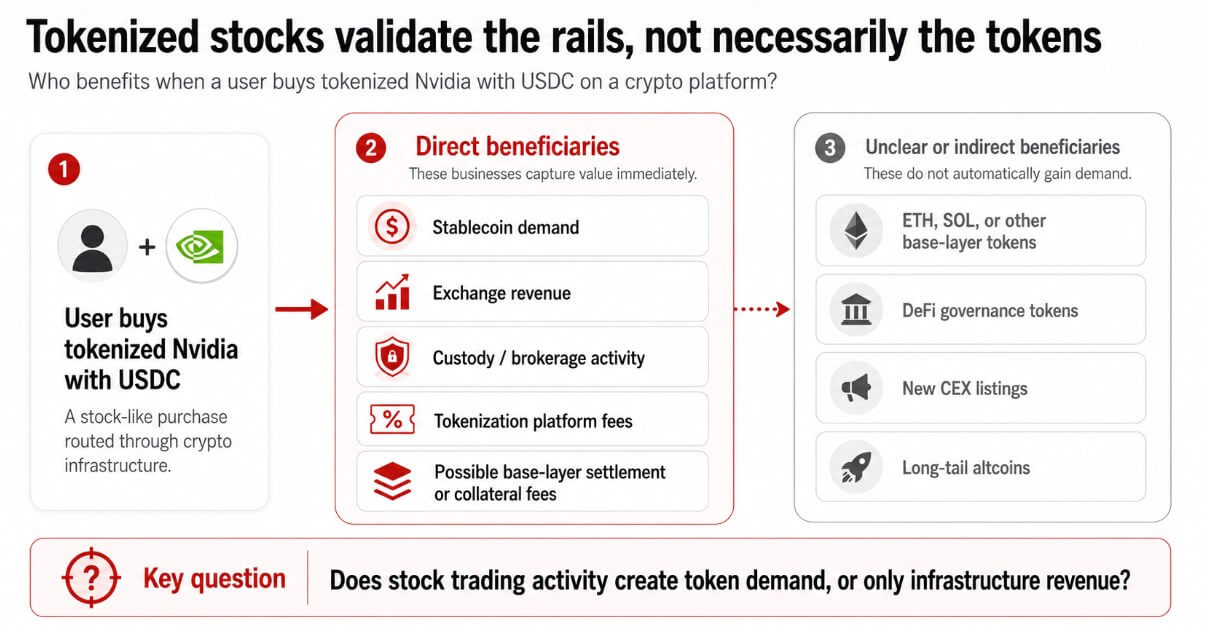

A user buying tokenized Nvidia with USDC creates demand for stablecoin settlement, exchange revenue, custody activity, and tokenization platform fees.

If stock trading activity routes through base-layer networks for settlement or collateral, select protocols could capture fee and staking demand from equity flows that never touch a new token listing, expanding the total addressable market even if crypto asset adoption stagnates.

The Delphi data and what it says about demand

Numbers from a recent Delphi report show that exchanges spent the 2025 cycle listing hundreds of tokens that overwhelmingly destroyed retail capital, and the same platforms now offering Nvidia or Apple exposure are implicitly conceding that the native listing product lost user trust.

A retail user with a stablecoin balance can now buy tokenized exposure to a company with quarterly earnings, analyst coverage, and a familiar brand through the same account that previously offered only new token listings at a -82% median return.

Tokenized stocks give existing crypto account holders a competing asset class inside the same account, and if exchanges succeed in making that the primary growth product, they validate crypto rails while reducing the addressable demand pool for new token listings.

Institutional allocators rotating from Bitcoin ETFs into AI equities, and retail users in crypto apps choosing tokenized stocks over new listings, put the structural demand argument for long-tail tokens under simultaneous pressure from both ends of the capital stack.

Exchanges running that model become TradFi distributors on crypto infrastructure, capturing stock trading revenue while the native listing business shrinks to a secondary product.

Base layers may still benefit from settlement and collateral activity, but governance tokens, new altcoin listings, and assets without earnings or utility face a valuation problem that tokenized stocks make harder to ignore.

What the products actually are

Kraken says xStocks provide price exposure without shareholder rights such as voting, and Robinhood describes its Stock Tokens as derivative contracts that carry liquidity, currency, and counterparty risks.

The SEC warns that third-party and synthetic tokenized securities may not represent ownership of or contractual obligations tied to the underlying security, exposing holders to the risk of issuer or custodian bankruptcy.

Tokenized stocks may reduce friction and expand reach, but users in emerging markets buying stock-like exposure through a crypto exchange may discover during a market-stress event that they have held a synthetic product.

The infrastructure win and the ownership disconnect can coexist, and it matters most precisely when market conditions make it most relevant.

Where value actually accrues

Stablecoins, exchanges, custodians, and tokenization issuers capture value from tokenized stock activity regardless of whether crypto-native tokens benefit.

A user funding a tokenized Nvidia purchase with USDC through Kraken generates stablecoin demand, exchange revenue, and tokenization platform fees without generating demand for ETH, SOL, or any new altcoin listing.

A tokenized Nvidia purchase with USDC directly benefits stablecoins, exchanges, and custodians, while base-layer tokens, DeFi governance tokens, and new listings gain no automatic demand.

A tokenized Nvidia purchase with USDC directly benefits stablecoins, exchanges, and custodians, while base-layer tokens, DeFi governance tokens, and new listings gain no automatic demand.

The bull case for crypto tokens requires that stock trading activity creates collateral, settlement, or staking demand that flows through crypto-native assets.

That chain of value capture is commercially plausible but depends on product design choices that exchanges have not yet fully committed to.

Binance Research's $2 trillion base case and $5 trillion bull case describe capital flowing through crypto infrastructure without necessarily creating demand for crypto-native tokens, which depend on separate design choices that exchanges have not yet committed to.

The post Crypto’s killer app may be selling stocks after its own tokens failed retail appeared first on CryptoSlate.

You May Also Like

BTC Price Shaky Near $67K While Oil Surges on Middle East Tensions: What's Next? (April 2 Update)

One Of Frank Sinatra’s Most Famous Albums Is Back In The Spotlight

LIST: Bayanihan initiatives amid soaring oil prices