Qualcomm Stock Round-Tripped to $226 on an AI Data Center Bet. Could the June 24 Investor Day Settle It?

Key Stats for Qualcomm Stock

- Current Price: $226.11 (June 18, 2026 close)

- Target Price (Mid): ~$241

- Street Target: ~$183

- Potential Total Return: ~7%

- Annualized IRR: ~2% / year

- Earnings Reaction: +15.12% (April 29, 2026)

- Max Drawdown (1Y): 33.89% (April 7, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Qualcomm (QCOM) is a stock the market cannot agree on. Shares closed at $226.11 on June 18, up 6.17%, near the top of a 52-week range of $121.99 to $259.92. That calm price hides a violent year: QCOM fell 33.89% to its low on April 7, 2026, then clawed almost all of it back.

The argument is easy to state and hard to settle. Qualcomm is a mature smartphone chip business being repriced as an AI infrastructure company before it has shipped much AI infrastructure. Bulls see a diversification engine in automotive, IoT, and data centers. Bears see a handset franchise losing Apple and filling the gap with promises. Whether the data center revenue is real gets answered on June 24, when Qualcomm hosts its Investor Day.

An analyst who isn’t bullish just raised his target 60%

On June 5, JPMorgan’s Samik Chatterjee lifted his QCOM target to $265 from $160 and placed the stock on “Positive Catalyst Watch”, while keeping a Neutral rating. That combination is the story in miniature. A 60% target hike from someone unwilling to call the stock a buy says the recent selling may have been overdone, and that the upside hinges on what management says next.

His math is specific. He expects Qualcomm to outline data center revenue above $3 billion in fiscal 2027, scaling toward $35 billion by fiscal 2031, with non-handset markets contributing roughly 70% of revenue by then. Wells Fargo moved the same way, raising its target to $230 from $160.

Consensus, though, is not bullish. TIKR’s data shows 10 Buys and 2 Outperforms against 22 Holds, 3 Underperforms, and 2 Sells, with a mean Street target near $183, below today’s price. The bullish numbers are outliers, not the center. Even Chatterjee’s $265 still sees double-digit upside from here, which is why his Neutral rating tells you as much as his target does.

Qualcomm Drawdowns (TIKR)

Qualcomm Drawdowns (TIKR)

See historical and forward estimates for Qualcomm stock (It’s free!) >>>

What management already told us at Bernstein

Investors got a preview on May 27, when CEO Cristiano Amon laid out the data center strategy at the Bernstein Strategic Decisions Conference. He described three parts: CPUs, an XPU (an inference accelerator, meaning a chip built to run AI models rather than train them), and custom ASICs (chips designed for a single customer). The architecture does not need HBM (high-bandwidth memory, the costly stacked memory most AI accelerators rely on), which Amon framed as a cost and supply edge.

On timing, he was blunt: “Material has to be in the multiple billions of dollars. That’s really what it means.” He said Qualcomm pulled data center revenue forward into fiscal 2027, that ASIC shipments could start within calendar 2026 on a U.S. hyperscaler win, and that the $2.5 billion Alphawave deal supplied the missing connectivity IP. He also said these engagements would be operating margin accretive.

The handset reality is soberer. Amon called the market “artificially constrained by the memory situation,” with units down about 15% year-over-year on supply, not demand, and said Qualcomm can “see the bottom in Q3.” On Apple, the most-asked question, he would only say licensing is in “one of the most stable times” and pointed to the courts on the chip relationship. That is the gap the data center story has to fill.

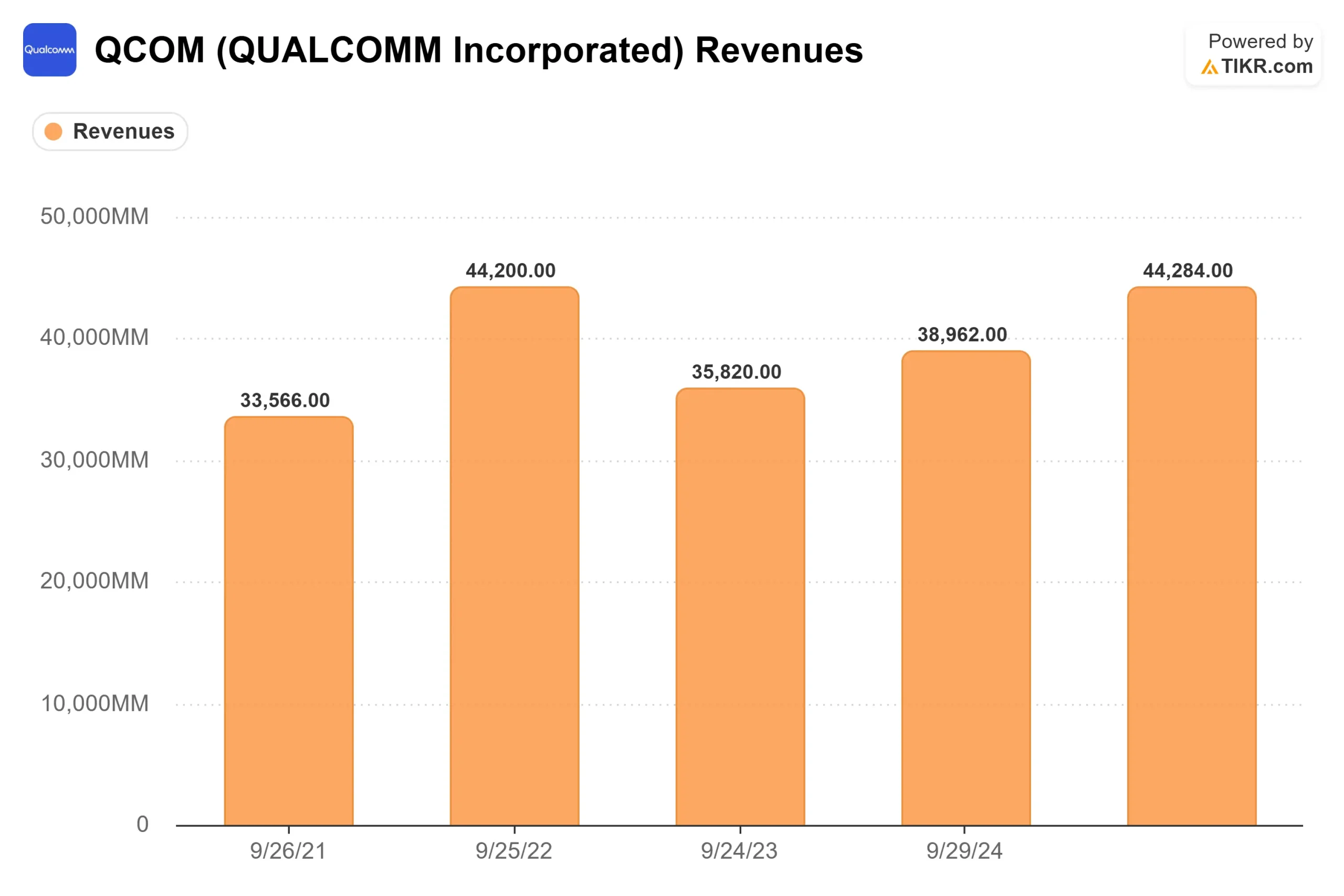

Qualcomm Revenues (TIKR)

Qualcomm Revenues (TIKR)

Qualcomm also trades cheaply against the bet it is being asked to win. On a next-twelve-months basis, QCOM trades at 5.99x EV/Revenues and a 23.14x P/E. The peers actually selling AI silicon trade far higher: NVIDIA at 11.64x NTM EV/Revenues, Broadcom at 14.14x, and Marvell at 21.53x. The market is still pricing QCOM as a wireless company. If Amon converts even part of the pipeline he described, that discount is the opportunity; if the Investor Day is vague, the discount is correct, because the handset cyclicality and the Apple headwind are real.

See how Qualcomm performs against its peers in TIKR (It’s free!) >>>

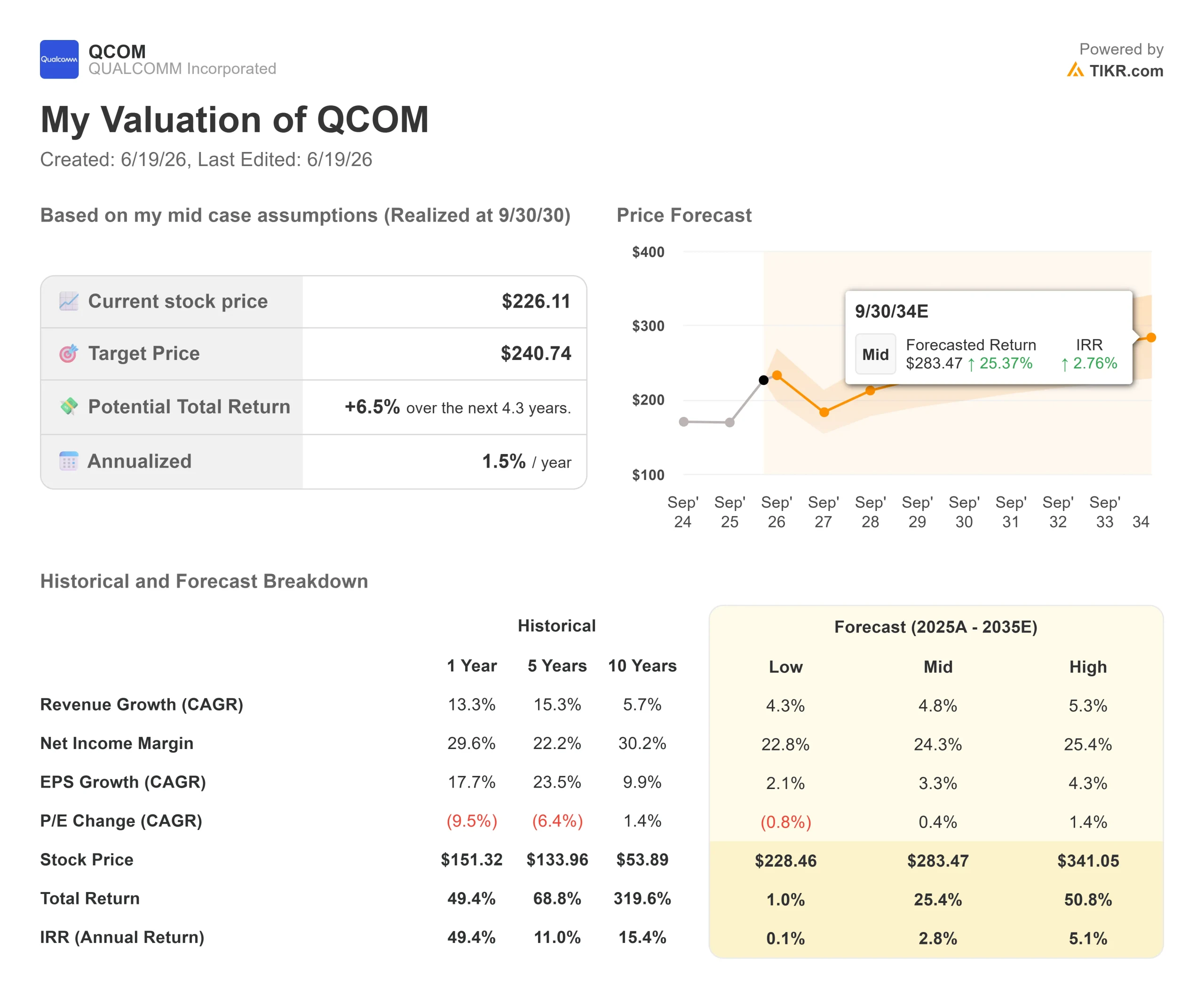

TIKR Advanced Model Analysis

- Current Price: $226.11

- Target Price (Mid): ~$241

- Potential Total Return: ~7%

- Annualized IRR: ~2% / year

Qualcomm Advanced Valuation Model (TIKR)

Qualcomm Advanced Valuation Model (TIKR)

See analysts’ growth forecasts and price targets for Qualcomm stock (It’s free!) >>>

TIKR’s mid-case, realized at September 30, 2030, lands on a target of around $241: roughly 7% total return and about 2% annualized over 4.3 years. At $226, the mid case alone does not justify chasing the stock here.

It rests on a forward revenue CAGR of around 5%, driven by two engines: automotive content growth as Qualcomm scales its digital cockpit and ADAS platforms, and the IoT recovery led by the personal AI device category Amon flagged, including smart glasses with 40-plus active designs. The margin driver is a net income margin holding around 24%, supported by the premium handset mix and the margin-accretive data center work. The primary risk is Apple, whose chip volume steps down with no product relationship confirmed beyond the current iPhone cycle.

The asymmetry is the point. The mid case offers around 7%, but the high case points to roughly $341 and about 51% total return if diversification compounds faster than the base assumes, while the low case sits near $228 with flat returns. That spread maps almost exactly onto the June 24 binary.

Conclusion

The whole stock comes down to one date. On June 24, Qualcomm has to put hard numbers behind the story Amon has been telling, and the bar is explicit: data center revenue tracking above $3 billion in fiscal 2027 and a credible path toward $35 billion by fiscal 2031, with dated hyperscaler shipments rather than ambition. Clear it with timelines and named commitments, and the rerating toward $265 has fuel. Deliver slideware, and the median $183 target wins. Watch the fiscal 2027 data center target above all else.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Qualcomm?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Qualcomm, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Qualcomm alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Qualcomm on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

Why Solana Amplified a Post on Unified Systems for Interoperability

Covéa Chooses Shift Technology as Strategic Partner for Fraud and Risk Management

One Of Frank Sinatra’s Most Famous Albums Is Back In The Spotlight