Lockheed Martin vs RTX: Which Defense Giant Is the Better Bet Amid Rising Tensions?

Key Takeaways

- Lockheed’s PAC-3 production is already up more than 60% in two years, with a new $4.8 billion contract signed and a tripling of output targeted under a seven-year Department of Defense framework agreement.

- RTX’s $271 billion backlog grew 25% year-over-year and its gross margins hold consistently above 20%, roughly double Lockheed’s, reflecting a commercial engine aftermarket that defense budget cycles cannot disrupt.

- Lockheed Martin stock trades nearly 23% below its 52-week high while its contract and demand backdrop has materially strengthened; RTX stock trades within 10% of its 52-week high with the model projecting minimal return from current prices.

- TIKR’s model targets $809 for Lockheed Martin stock at roughly 10% annualized, versus $218 for RTX stock at around 3% annualized, a four-to-one return gap from current prices.

Trying to decide between two defense giants? TIKR lets you pull up LMT and RTX side by side with the same institutional-grade financial data professional analysts use, for free →

Lockheed Martin vs RTX: Two Defense Business Models, One Investment Decision

Lockheed Martin (LMT) is the largest U.S. defense contractor by revenue, built around a concentrated portfolio of franchise platforms: the F-35 Lightning II (the only fifth-generation fighter in current production across the free world), PAC-3 interceptors, THAAD systems, JASSM cruise missiles, and the Precision Strike Missile, with roughly 95% of revenue coming directly from government contracts.

That concentration has become a strength in the current environment. CEO Jim Taiclet confirmed on the Q1 2026 earnings call that the F-35 performed escort and air-to-ground missions in operations against Iran’s nuclear infrastructure, with Taiclet noting the strikes “couldn’t have happened without them safely.”

The Patriot and THAAD interceptors provided layered air defense of civilian infrastructure across the Middle East theater, and those demonstrations of operational relevance are now converting directly into long-term production commitments.

Lockheed signed a seven-year framework agreement with the Department of Defense targeting a tripling of PAC-3 production, with a $4.8 billion fully funded contract already signed and more than 20 new facilities under construction to support the ramp.

The F-35 program, Lockheed’s single largest, saw the Pentagon request 85 aircraft in the fiscal year 2027 budget, up from 47 the prior year.

RTX Corporation (RTX) is a different kind of defense company. Where Lockheed Martin is a platform manufacturer, RTX is a systems integrator, engine maker, and munitions producer: Raytheon produces Patriot GEM-T, AMRAAM, Tomahawk, and NASAMS; Pratt & Whitney manufactures the F135 military engine and the GTF commercial engine powering much of the global narrow-body fleet; Collins Aerospace supplies avionics, interiors, and mission systems across both government and airline customers.

CEO Chris Calio reported 10% organic sales growth in Q1 2026 with all three channels contributing. CFO Neil Mitchill detailed that Raytheon munitions output was up more than 40% year-over-year, with the total backlog reaching a record $271 billion, up 25% year-over-year

RTX’s commercial engine business, particularly the GTF program with its 8,000-engine backlog, provides a compounding aftermarket stream Lockheed Martin simply does not have, with Pratt’s commercial aftermarket up 19% year-over-year in Q1.

The investment distinction comes down to this: Lockheed Martin stock is a leveraged bet on the defense spending supercycle, while RTX stock offers that same exposure layered with a commercial aviation cycle that adds a second compounding engine. That diversification is precisely why RTX commands a higher current valuation, and precisely why TIKR’s model shows a wider gap in the return potential available from each stock today.

Lockheed Martin’s munitions ramp and RTX’s record backlog are both moving fast. Track how analyst price targets for LMT and RTX are responding to each new contract award with TIKR for free →

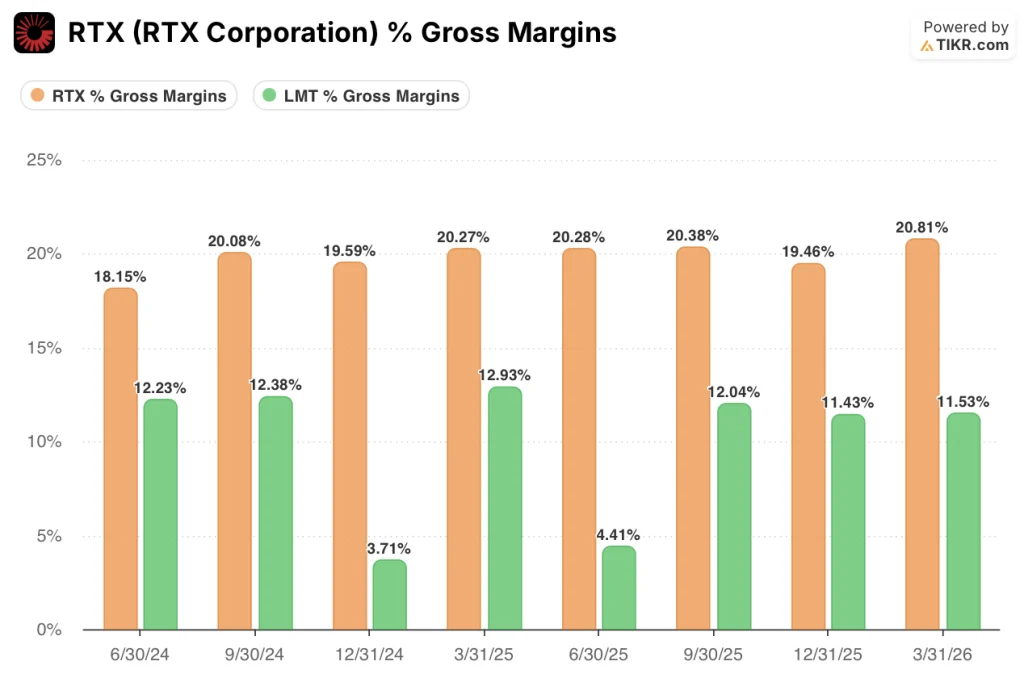

Lockheed Martin Has the Margin Pressure, RTX Has the Margin Structure

RTX Stock Gross Margins vs LMT Stock (TIKR)

RTX Stock Gross Margins vs LMT Stock (TIKR)

The clearest single number separating these two businesses is gross margin: RTX has posted above 20% consistently across the past eight quarters, reaching 21% in Q1 2026, while Lockheed Martin’s gross margins sit in the 11% to 13% range across the same period.

That gap reflects two fundamentally different cost structures. Lockheed operates primarily as a cost-plus contractor, where the government reimburses allowable costs and pays a negotiated fee, which limits gross margin expansion because revenue and cost lines move together.

RTX carries the same defense contracting exposure through Raytheon, but its commercial businesses, particularly Pratt’s engine aftermarket, operate with a structurally different profile: engine shop visits are high-margin, recurring, and largely non-discretionary for airlines that cannot ground their fleets, producing a blended gross margin roughly 9 percentage points above Lockheed’s.

RTX Stock Operating Margins vs LMT Stock (TIKR)

RTX Stock Operating Margins vs LMT Stock (TIKR)

At the operating line the divergence holds, with RTX posting 13% operating margins in Q1 2026, up from 12% a year earlier, versus Lockheed’s 11%, pressured by unfavorable adjustments on the F-16 and C-130 programs.

CFO Evan Scott attributed those specifically to a new Taiwan and Morocco F-16 configuration that hit rework costs and C-130 integration challenges from earlier in 2025, both now resolved, and both transitory rather than structural given that Lockheed’s operating margins reached 13% in Q2 2025 before those issues emerged.

RTX Stock Revenue Growth vs LMT Stock (TIKR)

RTX Stock Revenue Growth vs LMT Stock (TIKR)

Revenue growth tells a similar story: RTX grew 9% year-over-year in Q1 2026 with volume expansion across all three segments, while Lockheed’s Q1 2026 revenue was essentially flat, impacted by a shortened fiscal period and the same program timing issues management flagged.

RTX Stock Operating Cash vs LMT Stock (TIKR)

RTX Stock Operating Cash vs LMT Stock (TIKR)

On cash generation, RTX produced $1.86B in operating cash in Q1 2026 against LMT’s $0.22B, and while both businesses are structurally back-half loaded, RTX’s trailing four-quarter operating cash of around $11B runs well ahead of LMT’s roughly $7B, a gap that mirrors the margin structure separating them

The financial picture as of this quarter favors RTX on every headline metric, and the question the valuation model answers is whether that advantage is already fully priced in.

Lockheed Martin’s Discount Makes the Return Case While RTX’s Premium Erases It

TIKR’s model values Lockheed Martin at approximately $809, implying around 52% total return from the current price of approximately $532, or roughly 10% per year.

LMT Stock Valuation Model Results (TIKR)

LMT Stock Valuation Model Results (TIKR)

That target depends on Lockheed converting its backlog into deliveries at improving margins as the year progresses, with management guiding explicitly for margin gains in the second half of the year.

The 4% revenue CAGR assumption embedded in TIKR’s mid case is conservative relative to the demand signals visible in the order book, and if the munitions framework agreements convert into definitized contracts at the production rates targeted, the earnings power available by end of decade supports the target.

The condition that has to hold: Lockheed executes its production ramp without additional program charges on classified programs or further F-16 delays.

Meanwhile, TIKR’s model values RTX at approximately $218, implying around 13% total return from the current price of approximately $193, or roughly 3% per year.

RTX Stock Valuation Model Results (TIKR)

RTX Stock Valuation Model Results (TIKR)

That muted return projection does not reflect a weak business; it reflects a business the market has already largely recognized, with RTX’s record $271 billion backlog, 25% backlog growth, and consistent double-digit operating profit expansion priced into a stock trading near its 52-week high.

The commercial aftermarket cycle at Pratt, with GTF MRO output up 23% year-over-year and shop visits still growing, provides durable compounding that TIKR’s 5% revenue CAGR assumption captures, and that stream continues regardless of quarter-to-quarter defense budget noise.

The condition that has to hold: commercial air traffic continues recovering and no structural deterioration hits airline demand for GTF shop visits.

The argument between Lockheed Martin stock and RTX stock ultimately hinges on one question: does RTX’s margin and diversification premium justify buying a stock with almost no modeled return cushion, when its less-diversified rival offers four times the annualized return at a meaningful discount to its recent highs?

For an investor choosing between these two today, TIKR’s model projects roughly 10% annualized return from Lockheed Martin stock versus roughly 3% from RTX stock, a gap that places the return burden entirely on RTX’s quality premium rather than its price.

Should You Invest in Lockheed Martin Corporation or RTX Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Lockheed Martin Corporation stock and RTX Corporation stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down for both companies.

You can build a free watchlist to track Lockheed Martin Corporation and RTX Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze LMT and RTX stock on TIKR for Free →

You May Also Like

Pacquiao insists Mayweather fight for real, shuns exhibition insinuation

Stakestone (STO) Soars: Token Surpasses $1.14 After Stunning 367% Rally

Fed Governor Calls For Strong Stablecoin Oversight As CLARITY Act’s Final Text Gets Delayed