Singapore’s Web3 Exodus: What’s Next?

By Aiden and Jay Jo

Source: Tiger Research

Compiled by: Vernacular Blockchain

summary

Singapore has attracted many Web3 companies with its flexible regulatory environment and is known as the "Delaware of Asia". However, the proliferation of shell companies and the collapse of high-profile companies such as Terraform Labs and 3AC have exposed regulatory loopholes.

In 2025, the Monetary Authority of Singapore (MAS) will implement the Digital Token Service Provider (DTSP) framework. All companies providing digital asset services in Singapore must obtain a license. Simply registering a company will no longer be sufficient to conduct digital asset business.

Singapore continues to support innovation, but regulation has increased significantly, with the government requiring greater accountability and compliance. Web3 companies in Singapore need to develop operational capabilities or consider moving to other jurisdictions.

1. Changes in Singapore’s regulatory environment

For many years, global companies have called Singapore the "Delaware of Asia" for its clear regulations, low corporate tax rates and fast registration process. This foundation also applies to the Web3 industry. Singapore's business-friendly environment naturally makes it an ideal destination for Web3 companies. MAS recognized the growth potential of cryptocurrencies early and took the initiative to develop a regulatory framework to provide space for Web3 companies to operate within the existing system.

MAS enacted the Payment Services Act (PSA) to bring digital asset services under a clear regulatory system and launched a regulatory sandbox to allow companies to experiment with new business models under certain conditions. These measures reduced early market uncertainty and made Singapore the hub of the Web3 industry in Asia.

However, there has been a change in Singapore's policy direction recently. MAS has gradually abandoned its flexible regulatory approach, tightened regulatory standards and revised its framework. The data clearly shows this shift: the approval rate of more than 500 license applications since 2021 is less than 10%. This shows that MAS has significantly raised its approval standards and adopted stricter risk management measures under limited regulatory capacity.

This report explores how these regulatory changes are reshaping the Web3 landscape in Singapore.

2. DTSP framework: why is it launched now and what has changed?

2.1. Background of Tightened Regulation

Singapore saw the potential of the crypto industry early on and attracted a large number of companies through flexible regulations and sandboxes, so many Web3 companies consider Singapore as their Asian base.

However, the limitations of the existing system have gradually become apparent. A key issue is the "shell company" model, where companies register entities in Singapore but actually operate overseas, taking advantage of regulatory loopholes in the Payment Services Act (PSA). At the time, the PSA only required companies that provided services to users in Singapore to obtain a license, and some companies circumvented this requirement by operating overseas. These companies took advantage of Singapore's institutional credibility while evading actual supervision.

MAS believes that this structure makes it difficult to enforce anti-money laundering (AML) and counter-terrorism financing (CFT). Although the company is registered in Singapore, its operations and capital flows are completely overseas, making it difficult for regulators to implement effective supervision. The Financial Action Task Force (FATF) calls this the "offshore virtual asset service provider (VASP)" structure, warning that the inconsistency between the place of registration and the place of operation leads to global regulatory loopholes.

The collapse of Terraform Labs and Three Arrows Capital (3AC) in 2022 brought these issues to life. The two companies registered entities in Singapore but actually operated overseas, and MAS was unable to effectively supervise or enforce them, resulting in billions of dollars in losses and Singapore's regulatory credibility was damaged. MAS decided that it would no longer tolerate such regulatory loopholes.

2.2. Key changes and impacts of DTSP regulations

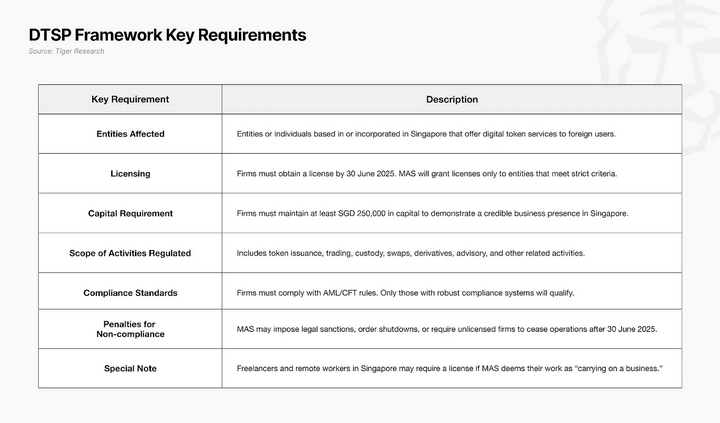

The Monetary Authority of Singapore (MAS) will implement new Digital Token Service Provider (DTSP) regulations from June 30, 2025, under Part IX of the Financial Services and Markets Act (FSMA 2022). FSMA integrates MAS's previously decentralized regulatory powers to form comprehensive financial legislation to cope with the new financial environment, including digital assets.

The new regulations are designed to address the limitations of the PSA. The PSA only requires companies that provide services to users in Singapore to obtain a license, and some companies have circumvented regulation by operating overseas. The DTSP framework directly targets this structural circumvention behavior, and all digital asset companies that use Singapore as an operating base or conduct business in Singapore must obtain a license, regardless of where their users are located. Even companies that only serve overseas customers must comply if they operate in Singapore.

MAS has made it clear that it will not issue licenses to companies that do not have a substantial business foundation. Companies that have not met the requirements by June 30, 2025 must cease operations immediately. This is not just a temporary enforcement, but a signal of Singapore's long-term transformation into a trust-centered digital financial center.

3. Redefinition of the scope of supervision under the DTSP framework

The DTSP framework requires digital token service operators in Singapore to comply with clearer regulatory requirements. MAS requires any business deemed to be "based in Singapore" to obtain a license, regardless of the location of its users or its organizational structure. Previously unregulated business types are now included in the regulatory scope.

Key examples include: companies registered in Singapore but operating entirely overseas; and companies registered overseas but with core functions (such as development, management, marketing) in Singapore. Even Singapore residents who participate in projects in an ongoing commercial manner may be subject to DTSP requirements, regardless of whether they are affiliated with a formal organization. MAS's judgment criteria are clear: Does the activity take place in Singapore? Is it of a commercial nature?

These changes not only expand the scope of regulation, but also require operators to have substantial operational capabilities, including anti-money laundering (AML), counter-terrorism financing (CFT), technical risk management and internal controls. Operators need to assess whether their activities in Singapore are regulated and whether they can maintain their business under the new framework.

The implementation of DTSP shows that Singapore is transforming itself from being a place that merely takes advantage of its regulatory reputation. Singapore now requires businesses to assume responsibility and discipline above a certain threshold. Companies and individuals who wish to continue to conduct crypto business in Singapore must have a clear understanding of their activities, recognize the regulatory implications under the DTSP standards, and establish appropriate organizational structures and operating systems when necessary.

4. Conclusion

Singapore's DTSP regulations show a change in the regulator's attitude towards the crypto industry. MAS previously maintained a flexible policy to help new technologies and business models quickly enter the market. However, this regulatory reform is not just a simple tightening, but imposes clear responsibilities on entities that use Singapore as their actual business base. The framework shifts from an open experimental space to only supporting operators that meet regulatory standards.

This change means that operators must fundamentally adjust their operations in Singapore. Companies that cannot meet the new regulatory standards may face a difficult choice: adjust their operating framework or relocate their business base. Places such as Hong Kong, Abu Dhabi and Dubai are developing crypto regulatory frameworks in different ways, and some companies may consider these regions as alternative bases.

However, these jurisdictions also require licensing for local users or services operating within their borders, involving capital requirements, anti-money laundering standards and substantive operational rules. Therefore, companies should consider migration as a strategic decision rather than a simple regulatory avoidance, and need to comprehensively consider regulatory intensity, regulatory methods and operating costs.

Singapore's new regulatory framework may create barriers to entry in the short term, but it also indicates that the market will be restructured around operators with sufficient accountability and transparency. The effectiveness of the system depends on whether these structural changes are sustainable and consistent. The future interaction between institutions and the market will determine whether Singapore can be recognized as a stable and reliable business environment.

También te puede interesar

MoneyGram puts stablecoins at the core of its next-generation app

Bu Altcoinin MicroStrategy’si Olmaya Çalışan Dev şirket, 4 Milyar Dolarlık Ek Altcoin Satın Almak İçin SEC’e Başvurdu!