There’s no universally accepted classification for tokenized stocks yet, but they can generally be grouped into several categories.

Asset-Backed

Each tokenized stock is backed by a real asset held by a custodian. While this setup ensures that the token is collateralized, it also requires a high level of trust in both the issuer and the entity responsible for safeguarding the underlying shares.

One example of this model is xStocks by Backed Finance — a Swiss company that acts as both issuer and custodian. The tokens are backed by actual shares, and any dividends are automatically reinvested into the tokenized asset.

Since these tokens can be traded 24/7, while traditional stock exchanges operate on fixed schedules, price discrepancies can occur. During market hours, such gaps are usually corrected through arbitrage. But after hours, those divergences often persist until the next trading session.

Synthetic

Synthetic tokenized stocks are not backed by real shares. Instead, they use smart contracts and price oracles to mirror the value of an underlying asset. In many cases, users are required to lock up collateral — usually in stablecoins — to maintain price stability.

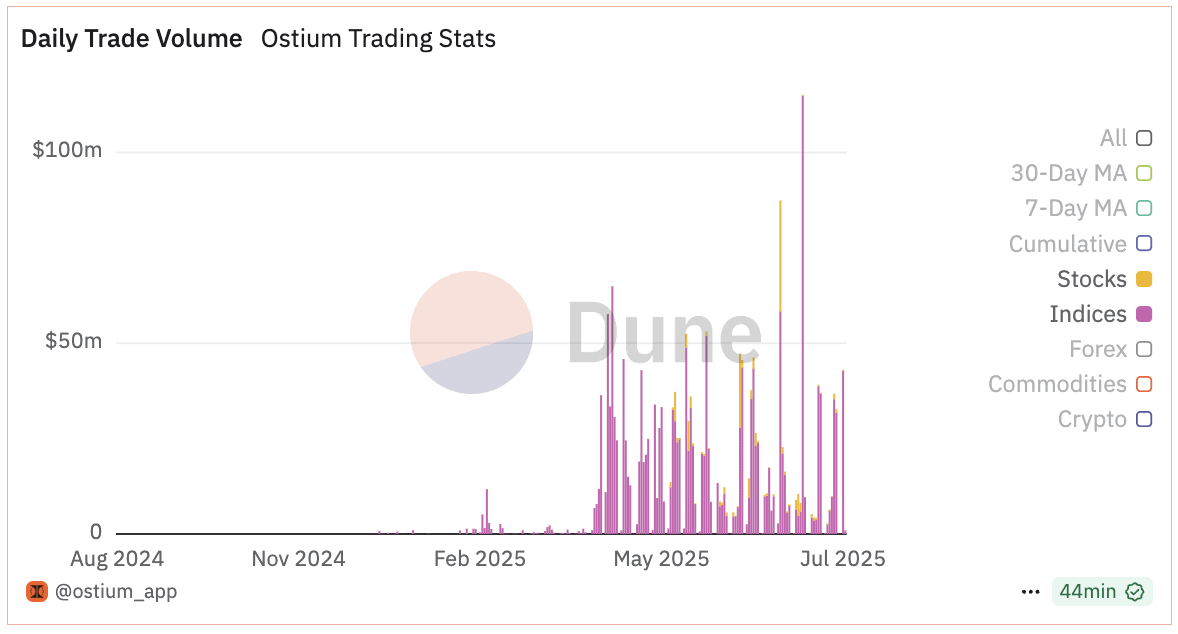

One example is Ostium, a platform built on Arbitrum that enables users to trade synthetic versions of traditional assets through perpetual futures.

Indirect Exposure via SPVs (private equity)

Robinhood recently announced support for tokenized assets tied to private companies like OpenAI and SpaceX.

These tokens aren’t actual shares and don’t carry legal shareholder rights. Instead, they’re backed by Robinhood’s ownership in a Special Purpose Vehicle (SPV) — a legal entity created specifically to hold equity in the private company.

This setup gives investors indirect exposure to pre-IPO companies. However, the structure relies on a relatively opaque SPV framework, which introduces both legal and regulatory risks.

Ownership in private companies is typically limited to closed investment rounds, venture capital funds, or specialized legal structures known as Special Purpose Vehicles (SPVs).

An SPV is a separate legal entity designed to isolate financial risk. Multiple investors can participate in an SPV to jointly hold assets such as stocks, bonds, or other securities.

According to Robinhood CEO Vlad Tenev, the platform acquires shares in private companies through SPVs and then issues tokens pegged to those holdings.

However, questions remain. It’s still unclear how Robinhood gains access to these private equity stakes — and there have been no public disclosures detailing the SPV structure or the legal framework surrounding ownership.

However, OpenAI stated that it does not endorse the launch of these tokens and is not affiliated with Robinhood’s initiative. In response, Vlad Tenev clarified that the tokens are not legally considered shares but do provide exposure to the securities of private companies.

Native

In this model, shares (or fractions of shares) are issued directly on the blockchain without duplication in traditional registries — the token itself is the security. This approach removes intermediaries and eliminates the need to reconcile data between the blockchain and external systems.

Issuing and managing such blockchain-based securities requires strict compliance with financial regulations. The issuer must ensure transparency of ownership, adhere to KYC/AML requirements, and complete necessary registration procedures.

A notable example is Exodus Movement Inc., the developer behind the Exodus crypto wallet. In June 2021, the company issued its shares as EXIT tokens on the Algorand blockchain via the Securitize platform.

Later, these securities started trading over-the-counter on the OTCQX market under the ticker EXOD, and from May 9, 2024, they were listed on the New York Stock Exchange (NYSE). On-chain trading of the tokens remains available through Securitize.

The variety of issuance methods highlights ongoing efforts to create efficient tokenization tools.

The motivation is clear — providers who can attract users from jurisdictions without direct access to the U.S. stock market stand to gain significant advantages.

But tokenization’s potential extends beyond this single challenge.

Trading Tesla tokens on Ostium is unavailable while the stock market is closed. Source: Ostium

Trading Tesla tokens on Ostium is unavailable while the stock market is closed. Source: Ostium

Tokenized Stocks Market Structure. Source: RWA.xyz

Tokenized Stocks Market Structure. Source: RWA.xyz

Trading Volumes of xStocks Tokenized Shares. Source: Dune

Trading Volumes of xStocks Tokenized Shares. Source: Dune

Trading Volumes of Stocks and Indices on Ostium. Source: Dune

Trading Volumes of Stocks and Indices on Ostium. Source: Dune