Is Datadog Stock a Buy After Raising Full-Year Guidance by $240 Million?

Key Takeaways for Datadog Stock as of June 2026

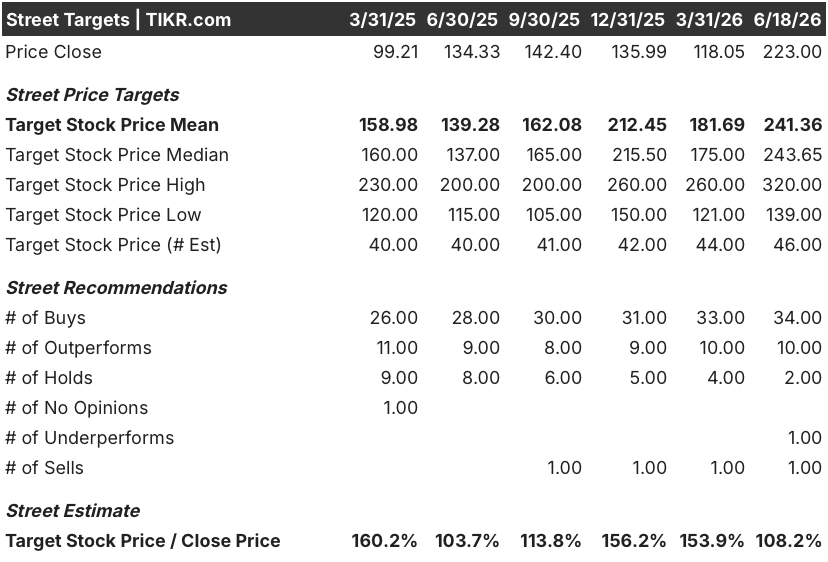

- Analysts rate Datadog stock 34 Buys, 10 Outperforms, 2 Holds, 1 Underperform, and 1 Sell, with a street mean target of $241 and a street high target of $320, implying around 8% upside to mean and around 43% to the high from the current price of $223.

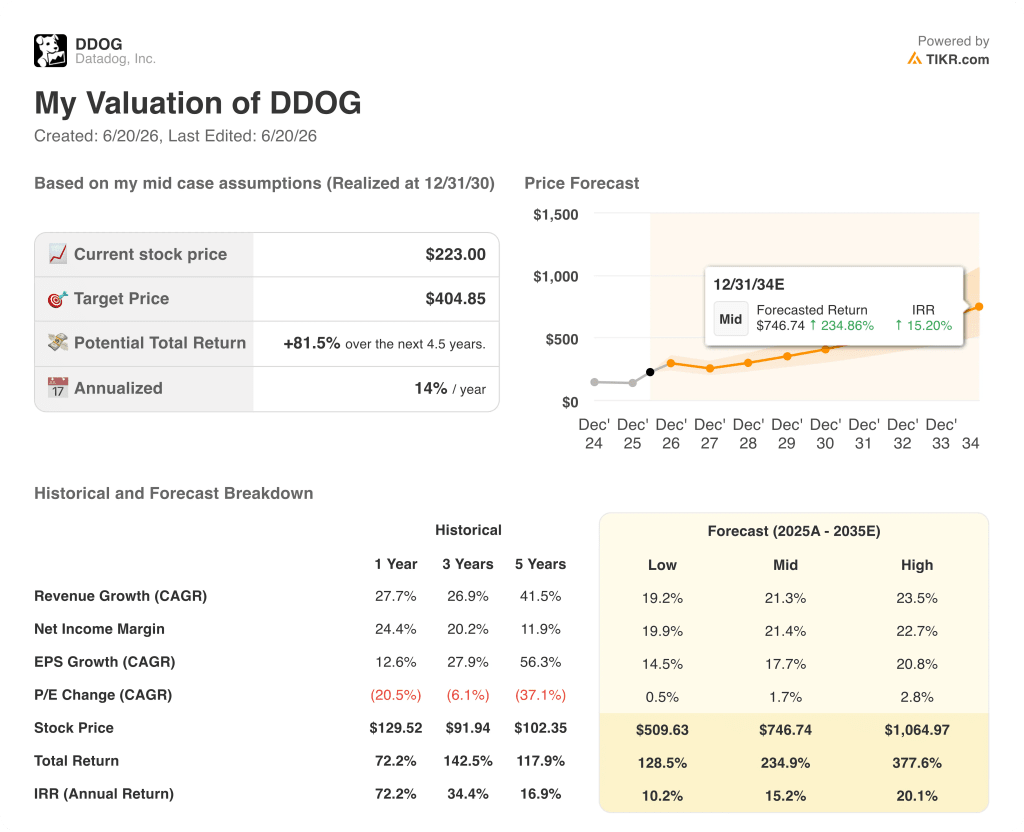

- TIKR’s mid-case model values Datadog at around $405 by December 2030, implying around 82% total return from current levels, or roughly 14% annualized over 4.5 years.

- Datadog stock delivered Q1 revenue of $1.006 billion, up 32% year over year, beating consensus by nearly 5% and prompting a full-year revenue guidance raise to $4.30 billion to $4.34 billion, a range well above prior guidance of $4.06 billion to $4.10 billion.

- Following its June DASH conference, Truist upgraded Datadog stock from Hold to Buy with a $300 target and Scotiabank raised its target to $275, with both firms citing accelerating enterprise AI adoption as the primary driver.

Datadog stock trades at $223 with 46 of 48 analysts bullish and a TIKR mid-case pointing to around $405 by 2030. Explore the revenue trajectory and analyst targets driving that gap on TIKR for free →

Datadog Hits $1 Billion Quarterly Revenue and Raises Full-Year Guidance on AI Surge

Datadog (DDOG) crossed the $1 billion quarterly revenue threshold for the first time in Q1 2026, delivering $1.006 billion in revenue, up 32% year over year and ahead of the $960 million consensus estimate.

DDOG Stock Q1 2026 Earnings in USD (TIKR)

DDOG Stock Q1 2026 Earnings in USD (TIKR)

Revenue growth accelerated for the third consecutive quarter, moving from 25% in the year-ago period to 29% last quarter to 32% in Q1, a trajectory that surprised even the most bullish analysts on the call.

The acceleration was not concentrated in a single segment: non-AI customer revenue grew at a mid-20s percentage rate year over year, up from 23% the prior quarter and 19% in the year-ago quarter.

Large customers powered the gain, with customers generating $100,000 or more in annual recurring revenue climbing 21% year over year to approximately 4,550 as of March 31, 2026.

Product adoption deepened alongside revenue, with 35% of customers now using six or more Datadog products, up from 28% a year ago, and 20% using eight or more products, up from 13%.

CEO Olivier Pomel told analysts on the Q1 earnings call: “We are helping customers of all sizes and industries deploy modern, cloud-based, AI-enabled solutions.”

Datadog’s Bits AI Security Agent, which autonomously investigates cloud SIEM signals and delivers remediation recommendations in as little as 30 seconds rather than hours, emerged as a breakout product this quarter, with significant expansion wins at a Fortune 500 bank and a leading online recruiting platform.

The company also landed its first 8-figure annualized training-workload deals with the AI research divisions of two of the world’s largest technology companies, expanding the addressable market from inference into GPU-intensive model training at hyperscale.

Net revenue retention for the trailing twelve months moved to the low 120% range, up from approximately 120% the prior quarter, and free cash flow reached $289 million with a 29% margin, both figures pointing to a business operating with financial discipline alongside rapid expansion.

At the DASH user conference in New York on June 9 and 10, the company unveiled more than 100 new capabilities, including autonomous Bits AI agents, AI Guard for agentic security, Bring Your Own Cloud deployment, and new agent-building tools designed for enterprise AI workflows.

Track Datadog stock’s customer growth, ARR momentum, and AI product pipeline as Q2 estimates approach on TIKR for free →

Why 44 of 48 Analysts Are Bullish on Datadog Stock Right Now

Street Analysts Target for DDOG Stock (TIKR)

Street Analysts Target for DDOG Stock (TIKR)

Wall Street rates Datadog stock overwhelmingly bullish, with 44 of 48 analysts holding Buy-equivalent ratings following the Q1 results and subsequent DASH conference, where the company’s agentic AI roadmap landed as a significant catalyst.

DDOG Stock Revenue and EBITDA Actuals & Estimates (TIKR)

DDOG Stock Revenue and EBITDA Actuals & Estimates (TIKR)

Consensus even expects Datadog stock’s revenue to reach around $1.08 billion in Q2, up approximately 30% year over year, sustained by the same broad-based customer expansion and AI workload adoption that drove Q1.

Looking further out, the Street projects revenue of around $1.11 billion in Q3 and around $1.15 billion in Q4, implying full-year 2026 revenue growth of around 27%, consistent with management’s raised guidance midpoint.

EBITDA growth tells the margin story: Q1 EBITDA came in at $241.42 million, a 36% year-over-year gain, with consensus expecting roughly $260 million in Q2, representing approximately 47% year-over-year growth.

Truist, in its June 15 upgrade from Hold to Buy with a $300 price target, argued that urgency in enterprise AI adoption has begun outweighing optimization pressure, and that customers “remain early in their agentic AI journeys,” meaning the platform’s usage-based revenue model sits at an early point on a long adoption curve.

The open question for analysts is whether the DASH product announcements, particularly AI Guard and Bring Your Own Cloud, will accelerate the attach rate of higher-margin security products to Datadog’s existing observability base before the Q2 print.

Is Datadog Stock Undervalued in 2026? TIKR’s $405 Target and the AI Workload Condition

TIKR’s mid-case values Datadog at approximately $405 by December 2030, implying around 82% total return from the current price of $223, or roughly 14% annualized over 4.5 years.

DDOG Stock Valuation Model Results (TIKR)

DDOG Stock Valuation Model Results (TIKR)

The revenue trajectory established in Q1, where Datadog crossed $1 billion quarterly for the first time and raised full-year guidance to the $4.30 billion to $4.34 billion range, provides the growth foundation the mid-case target requires.

If the non-AI customer base continues its multi-quarter acceleration toward the mid-20s percentage growth rate, while AI native customers sustain their pace and the new training-workload vertical gains further penetration, the mid-case revenue CAGR of around 21% through 2030 is achievable without requiring the bull case assumptions on AI spending to fully materialize.

The condition the TIKR target depends on most directly is the durability of EBIT margin expansion alongside revenue growth: Q1 confirmed that operating expenses can grow at 31% while revenue grows at 32%, and sustaining that operating leverage through the company’s continued go-to-market investment cycle is what makes roughly 14% annualized returns reachable from current prices.

Datadog’s TIKR model targets around $405 by 2030. Pull the full model, check every assumption, and decide if the AI workload thesis holds on TIKR for free →

Should You Invest in Datadog, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Datadog, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Datadog, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze DDOG stock on TIKR for Free →

What is the biggest risk to the Datadog stock bull case?

The largest near-term risk is concentration in AI-native spend: management applied a higher degree of conservatism in Q2 guidance to its single largest customer, suggesting some caution around top-of-funnel volatility in frontier AI budgets. If enterprise optimization cycles return and reduce consumption on the platform, the Q3 and Q4 estimates of around $1.11 billion and around $1.15 billion in revenue could face pressure.

추천 콘텐츠

Widow’s Two-Year Tax Window on Home Sale Could Save $250,000 in Capital Gains

Furious right-wing Italian paper brands Trump with a vulgar term in scorching op-ed

EUR/GBP Exchange Rate Surges as Bank of England Rate Hike Expectations Intensify – Market Analysis

인기 뉴스

더보기