The 6% security gap: How Nigerians protect savings using their fintech apps

Only 6% of Nigerians say they feel financially secure. That number comes from the Piggyvest Savings Report 2025, a survey of more than 26,000 people across all six geopolitical zones, and it sits alongside another 6% from a completely different source.

Yet, Credit Direct’s Nigeria Credit Landscape Report 2025 found that only about 6% of Nigerian adults currently access credit through formal financial institutions, even though more than 64% are considered financially included.

Two separate surveys, built from different methodologies and asking different questions, arrive at the same 6% floor.

One measures how people feel about their money. The other measures whether the financial system will actually lend to them when they need it. Together, they describe a country where opening a bank account has stopped being the hard part and where the real gap sits somewhere between having access and having security.

Read also: From ‘urgent ₦2k’ to real credit: How Oxygen X wants to help Nigerians breathe

Too few to count

To help you understand, 6% is just 14.5 million people out of an assumed UN population guess of 242 million.

The Piggyvest report found that over 50% of Nigerians begin every month unsure whether their income will cover basic expenses. More than half of income-earning respondents said they provide financial support to extended family, a practice often called black tax, which quietly drains disposable income before any of it reaches a savings account.

Preliminary projections from major economic research firms indicate that headline inflation in June will likely hover around 15.8% to 15.95%, a slight shift from the 15.93% recorded in May 2026, continuing a year-long decline after monetary tightening and exchange rate reforms. Yet food inflation rose again to 16.96% month on month in May, reversing a brief dip to single digits in January.

The policy numbers are moving in the right direction. The lived experience is not catching up at the same pace, and that gap is exactly what pushes ordinary Nigerians toward fintech tools that promise to do what a savings account used to do on its own.

The credit side of the story compounds the problem. Credit Direct found that credit to Nigeria’s private sector stands at just 13.1% of GDP, far below comparable economies such as Kenya and South Africa, and that microfinance banks account for only 5.4% of the country’s total loan book. Traditional commercial banks continue to guard their loan books tightly, which means the vast majority of Nigerians who face a medical emergency, a business disruption, or a sudden loss of income have no formal credit line to fall back on.

A single shock can erase years of saved progress, and with formal credit largely out of reach, whatever cushion exists has to be built manually, one deposit at a time, through tools outside the traditional banking system. This is the environment in which Nigeria’s fintech platforms have become something closer to a financial defence mechanism than a convenience.

The country’s payment infrastructure has grown fast enough to support that shift. Electronic payment transactions in Nigeria surged to an all-time high in 2025, reaching about ₦1.2 quadrillion, while Point-of-Sale (PoS) transactions in Nigeria reached historic heights in 2025, with total transaction value hitting ₦38.01 trillion in the first eight months alone.

That volume of activity shows a population that has largely moved its everyday transactions onto digital rails, and increasingly, onto digital savings rails as well, in search of the protection a traditional account no longer provides.

Do fintechs help Nigerians save?

The numbers behind that protection are real, even if they take some work to unpack.

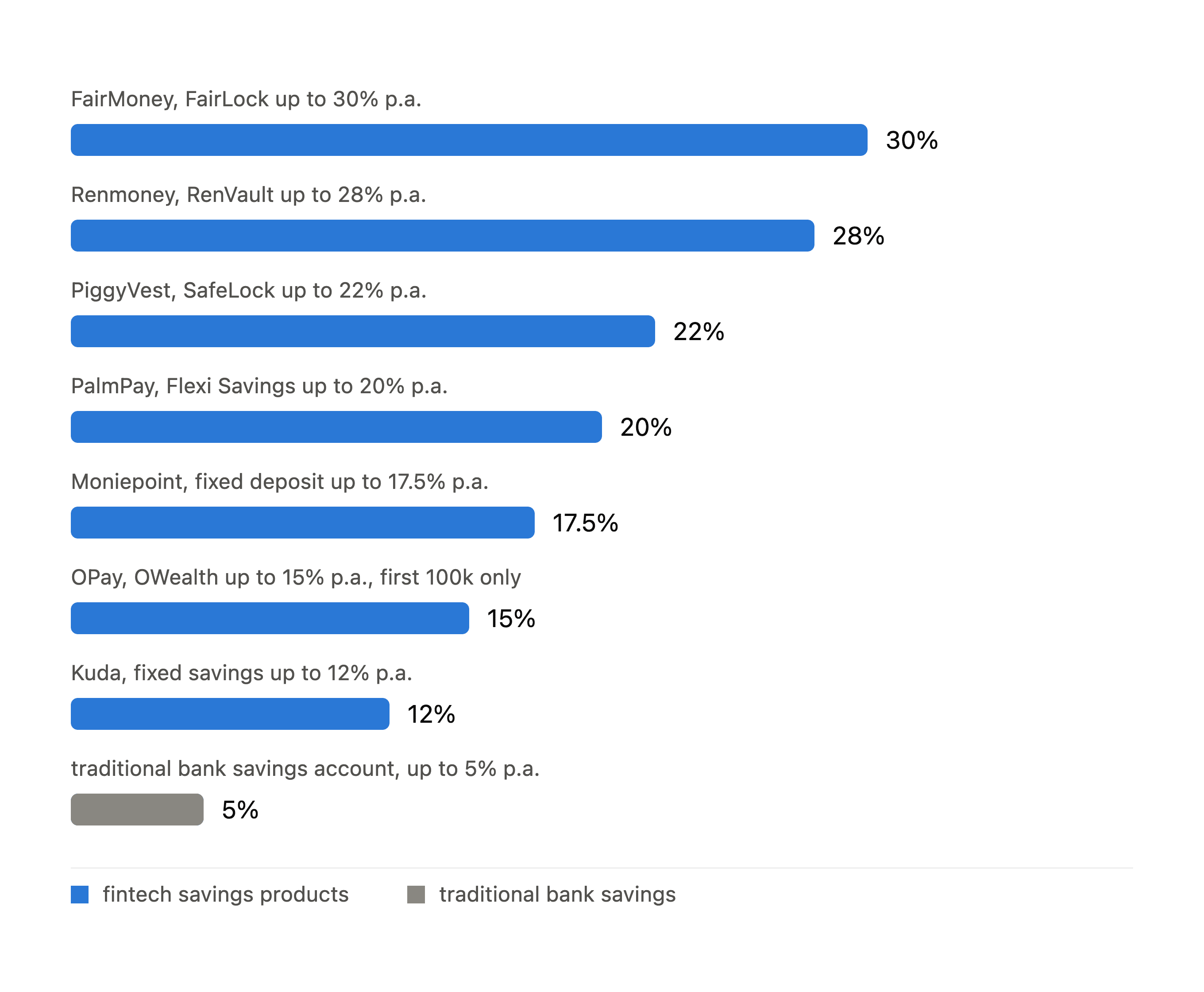

Piggyvest currently advertises up to 22% per annum on its core savings product, with its SafeLock feature paying between 14 and 22% depending on how long a user commits funds, across tenures from 10 to 1,000 days. Run through Piggyvest’s own calculator, a user saving ₦100,000 in daily instalments of ₦3,336 over a single month, say from July 6 to August 6, 2026, earns ₦821.92 in interest.

That is a modest sum on its own. Still, it is money that a traditional current account would never have generated at all, and it reflects the reality that building a meaningful shield through these products takes sustained daily discipline rather than a single lump deposit against a headline rate.

Other platforms carry the same logic, with returns that vary by product design in ways a saver has to actively track.

- Moniepoint pays 9.5% on flexible savings and up to 17.5% on fixed deposits.

- Kuda’s fixed savings plans sit between 10 and 12%, even as the platform separately advertises a 16% rate elsewhere on its own site, a discrepancy that underscores how much diligence ordinary savers now have to apply just to know what they are actually earning.

- PalmPay advertises up to 20% with no stated floor.

- Renmoney’s RenVault product offers up to 28%, depending on the size of the investment rather than simply the length of the lock-in period.

- FairMoney’s range runs from 13 to 30% depending on the specific plan, with its flexible FairSave product capped at 14% and its fixed FairLock product ranging from 17 to 28% depending on tenure.

- OPay’s OWealth product carries the same fine print. It pays up to 15% per annum, but only on the first ₦100,000 saved, with any balance above that threshold earning just 5% instead, which means a saver has to actually read the terms to know what their money is doing, rather than trusting the number on the homepage.

Nigeria fintech savings rates comparison

Nigeria fintech savings rates comparison

None of this changes the basic math in the saver’s favour. Even the lower end of these rates still comfortably outpaces what any traditional savings account pays, which is precisely why adoption of these products keeps climbing even as the fine print grows more complicated to navigate.

Alongside naira-denominated products, several platforms also offer dollar savings features built specifically to hedge against currency depreciation rather than to generate high returns.

FairMoney’s FairDollar product, for instance, pays a comparatively modest 6% on flexible United States dollar deposits. Its value lies in capital preservation against naira weakness, not in outpacing inflation the way a naira SafeLock or FairLock product claims to.

Read together, these fintech products describe two different survival strategies operating side by side. Naira-locked savings products are the closest thing many Nigerians have to yield, while dollar products exist to protect whatever value has already been saved from disappearing.

None of this activity is happening in a regulatory vacuum.

The Central Bank of Nigeria has set a target of 95% financial inclusion by 2028 under its Payments System Vision, a goal that would require bringing tens of millions of currently excluded adults into the formal system within roughly two years of that deadline.

Credit Direct’s own research suggests the harder problem may not be inclusion itself but what happens after someone is included. Financial inclusion in Nigeria has already climbed past 64%, yet only 6% of that included population can access formal credit, and only 6% of Nigerians overall report feeling financially secure.

Getting more people a fintech wallet or a bank account has proven to be the achievable part of the policy goal.

Making that access mean something, in the form of usable credit and a genuine cushion against shocks, is the part the numbers say Nigeria has not yet solved, and it is the part fintech savings products are currently being asked to fill in on their own.

추천 콘텐츠

Franklin Templeton CEO Dismisses 50bps Rate Cut Ahead FOMC

Robotics Automation Prototyping: Engineering Kinetic Agility into End-Effectors

Cryptocurrency scam losses hit $56.8 million in Texas! What are officials doing in response?

인기 뉴스

더보기