Bitcoin Crash To $30,000? China Mining Giant Says Strategy Can Survive

Jiang Zhuoer, CEO of BTCTOP and one of China’s best-known Bitcoin mining figures, pushed back against fears that Strategy could become a major forced seller of BTC, arguing that the company’s balance-sheet risk remains manageable even under a severe Bitcoin drawdown.

In a post on X, Jiang said he does not believe MicroStrategy, now Strategy, will “substantially net sell BTC,” pointing to a group discussion he shared on the company’s liabilities, STRC interest payments, funding structure and market concerns. The comments come as investors debate whether Strategy’s Bitcoin-backed capital markets model could come under pressure if BTC weakens further or if demand for STRC remains fragile.

Bitcoin Panic Over Strategy Overblown?

At the center of Jiang’s argument is the distinction between selling some Bitcoin and becoming a net seller of Bitcoin. He argued that a limited sale of older, low-cost BTC could be used to demonstrate realized investment gains, support STRC-related payments and reassure traditional investors without changing the broader accumulation strategy.

“MicroStrategy will not significantly net-sell its coins,” the translated group discussion stated. “He already explained the reason for the last coin sale in an interview. He wanted to sell STRC.”

According to the discussion, Strategy’s logic rests on the assumption that Bitcoin’s long-term appreciation can support the cost of STRC funding. The message attributed the thesis to a calculation that BTC can compound at around 30% annually, while using roughly 10% to pay interest would still leave sufficient room for the strategy to work.

The concern, however, is not simply whether Strategy owns enough Bitcoin. It is whether the firm’s financing structure looks credible to traditional investors. The discussion framed the market’s core worry bluntly: if later STRC proceeds are used to pay earlier STRC interest, critics could view the model as resembling a Ponzi-like funding loop.

That is why, in Jiang’s view, selective Bitcoin sales may be necessary rather than alarming. Selling some of the earliest and cheapest BTC would allow Strategy to show accounting gains. Those gains could then be used to pay STRC interest, while newly raised STRC proceeds are deployed into additional Bitcoin purchases. If the new BTC purchases are several times larger than the old BTC sold, Jiang argued, Strategy remains a net buyer.

“So MicroStrategy has to sell some of the earliest and cheapest Bitcoin it bought,” the translated discussion said. “That way, accounting-wise, it can show investment gains. Then using the investment gains from selling Bitcoin to pay STRC interest becomes completely reasonable.”

Jiang also pushed back against fears that Strategy’s liabilities could spiral if STRC trades below par. He said the current debt-to-asset ratio is only about 5%, and characterized STRC’s discount as a short-term market sentiment issue rather than a sign of insolvency risk. In the worst case, he argued, several months of continued payments could restore confidence in the instrument.

The discussion used a real estate analogy to explain the point. If a borrower owns $10 billion of houses and has borrowed $500 million, lenders may still worry if the borrower insists the houses can never be sold. But if the borrower shows willingness to sell one house to cover interest, the risk profile changes.

“After all, I have 10 billion worth of houses, and I only borrowed 500 million,” the translated message said. “As long as I’m willing to sell houses, there absolutely won’t be a situation where I can’t repay 500 million. That is why MicroStrategy has to start selling coins: to borrow more money and buy more coins.”

Jiang’s argument also distinguishes STRC holders from Bitcoin holders. In his view, STRC buyers are not primarily betting on BTC upside; they care whether Strategy is willing and able to pay dividends. If the company shows that it can monetize BTC when needed, that may reduce the biggest concern among STRC investors.

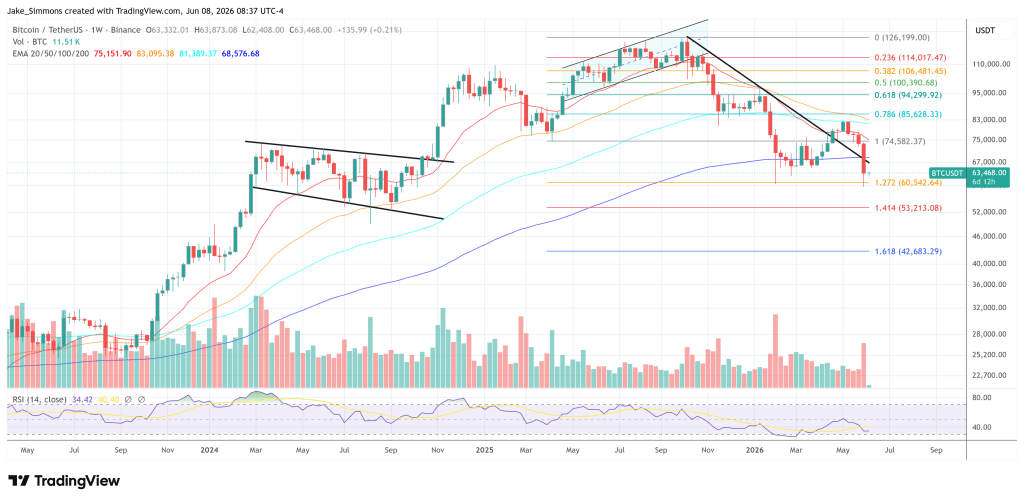

At press time, BTC traded at $63,468.

You May Also Like

Bernstein Says Bitcoin’s Quiet Cycle May Be Healthier Than It Looks

US forces’ odds of entering Iran by April 30 rise to 66% after Isfahan strike

U.S. Spot Ethereum ETFs Extend Inflow Streak to Two Days, Adding $68.17M