KLA Corp Stock Fell 9% and Analysts Still See Downside. Is KLAC Finally Cheap?

Key Stats for KLA Corp Stock

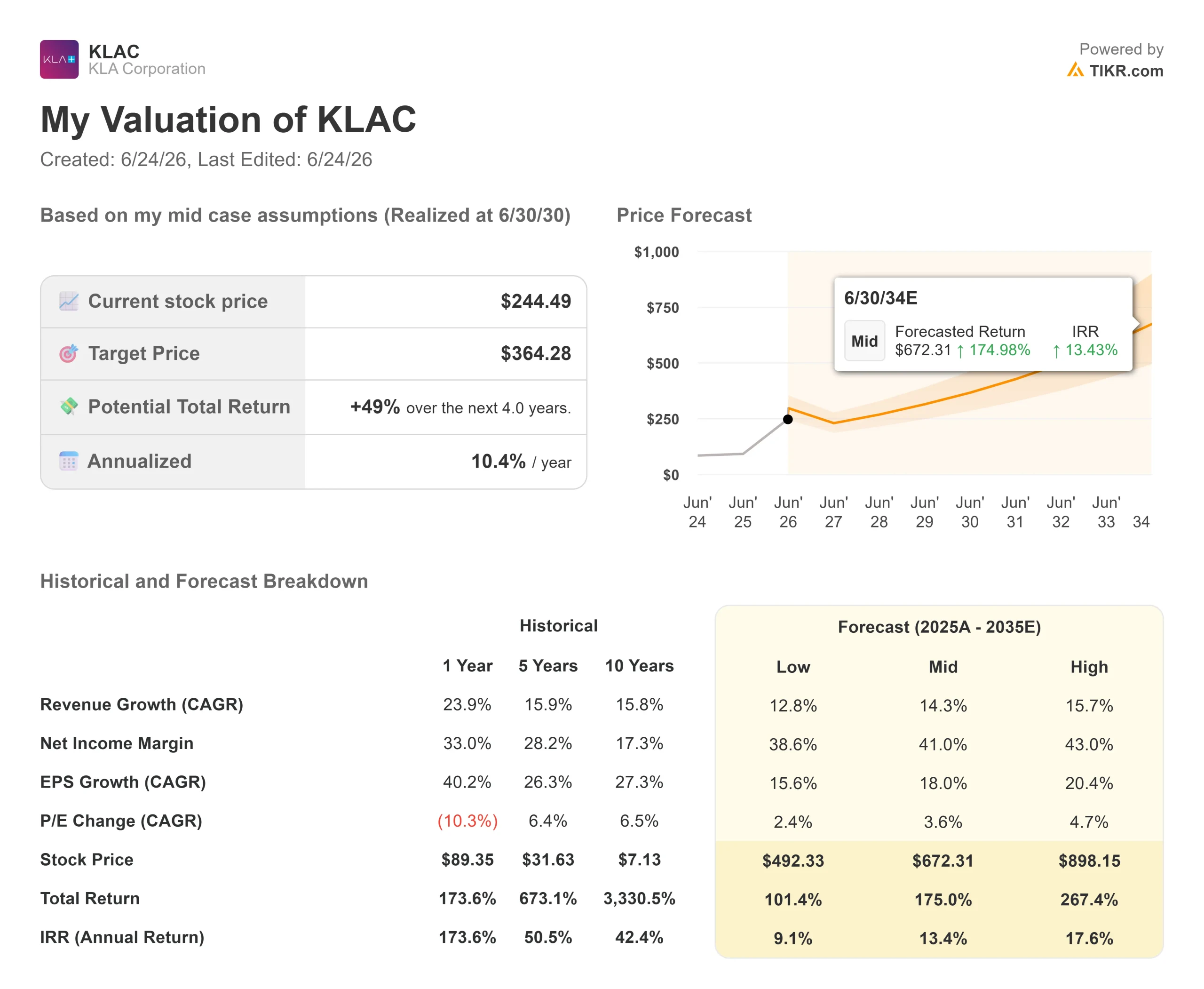

- Current Price: $244.49

- Target Price (Mid): ~$365

- Street Target: ~$205

- Potential Total Return: ~49%

- Annualized IRR: ~10% / year

- Earnings Reaction: -3.63% (April 29, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

KLA Corporation (KLAC) lost 9.17% on June 23, just one day after touching an all-time high. The drop had nothing to do with KLA. A report that South Korea’s SK Hynix is slowing its high-bandwidth memory ramp rattled the whole AI-chip complex, and KLA fell with the group.

That is the kind of move value hunters wait for: a great business knocked down on someone else’s news. Here is the catch. Even after the slide, the average analyst still sees KLA going lower. The mean target sits below today’s price. So the real question for KLA stock in 2026 is not why it fell. It is whether the fall made it cheap, or whether the Street was right that it was expensive.

KLA Corp Drawdowns (TIKR)

KLA Corp Drawdowns (TIKR)

See historical and forward estimates for KLA Corp stock (It’s free!) >>>

Why KLA Dropped When KLA Did Nothing

According to South Korean outlet Chosun Biz, SK Hynix is slowing its shift to next-generation HBM4, the stacked memory that feeds AI chips, and steering that capacity toward conventional DRAM, where shortages have pushed margins higher.

Investors read it as a crack in the AI-memory story. South Korea’s Kospi closed about 10% lower, SK Hynix and Samsung each fell more than 12%, and the selling spread to the US. KLA, which supplies inspection tools to those chipmakers, got pulled down with them.

The reaction looks harsher than the news. SK Hynix is making a margin choice, not cutting output. It is building different chips, not fewer of them. KLA’s tools inspect both kinds, so the shift barely touches demand for what KLA sells. The market sold first anyway, and that is what created the question worth examining.

The Problem Hiding Under the Headline

KLA stock in 2026 is hard to call because the business is excellent, and the stock still is not obviously cheap.

After the drop, KLA trades at a forward P/E near 51 times. That is a rich multiple for a company tied to a cyclical end market. The 10-for-1 split that took effect June 12 changed the share price, not the multiple, and the multiple is what bears are circling.

The clearest signal is the analyst data. The Street’s mean target is around $205, below the current $244.49. The breakdown runs 13 Buys, 5 Outperforms, 10 Holds, 1 Underperform, and 1 Sell. Direction skews bullish, but the targets say the average analyst sees the stock as already ahead of itself. When a 9% drop still leaves a price above consensus, the discount is shallower than the red suggests.

Bulls counter that the Street is anchored to a stale baseline. KLA topped revenue estimates in each of the last five quarters, so today’s targets may simply trail where estimates are heading.

What Management Said When It Mattered

The bull case got a clear airing this month. At the Bank of America Global Technology Conference on June 3, CFO Bren Higgins called the setup durable: “The year is shaping up to be a very good one for the company and for the industry on top of a couple of good years.” That pushes back on the cyclical-peak fear driving the selloff.

He addressed the memory worry directly, describing the environment as “very constructive over the next several quarters,” with customers focused on adding capacity, not trimming it. If that holds, the SK Hynix headline is noise.

Where KLA Sits Against Its Peers

KLA is the most expensive major name in its group, which is the heart of the debate. On TIKR’s Competitors page, it trades at an EV/EBITDA of 42.54 times, above Applied Materials at 33.88 times and ASML at 34.86 times, and roughly level with Lam Research at 42.13 times.

Is the premium earned? KLA’s gross margin of 61.4% is the best in the group, its share is rising, and its service business adds recurring revenue that peers cannot match. The bear reply is simpler: a premium multiple on a cyclical business leaves no cushion when sentiment turns, which is exactly what June 23 showed.

KLA Corp NTM (P/E) & NTM EV/EBITDA (TIKR)

KLA Corp NTM (P/E) & NTM EV/EBITDA (TIKR)

See how KLA Corp performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $244.49

- Target Price (Mid): ~$365

- Potential Total Return: ~49%

- Annualized IRR: ~10% / year

KLA Corp Advanced Valuation Model (TIKR)

KLA Corp Advanced Valuation Model (TIKR)

See analysts’ growth forecasts and price targets for KLA Corp stock (It’s free!) >>>

That is a solid return, not a deep-value bargain, which fits a strong business that fell on someone else’s news rather than a broken one.

The mid-case rests on two revenue CAGR drivers: rising process control intensity across AI logic, high-bandwidth memory, and advanced packaging; and steady share gains near 50 basis points a year. The margin driver is gross margin, climbing from about 62% toward management’s 63% to 64% target. The main risk is China, roughly a third of fiscal 2025 revenue, where export controls are tightening.

Upside: if the cycle runs as long as management implies, earnings beat the mid-case and the stock re-rates.

Downside: if growth cools, the multiple resets toward the Street’s sub-$205 target.

Conclusion

The honest answer is cheaper, not cheap. A 9% drop on a Korean margin story does not dent the franchise, but it does not pull the price below where the average analyst thinks it belongs either. The mid-case points to roughly 10% a year, which rewards patience without promising a windfall.

The number that settles it comes July 30, when KLA reports fiscal Q4 2026 against guidance of about $3.575 billion in revenue. A print at or above that, with second-half supply constraints easing, makes the post-drop price look like the discount bulls claim. A miss hands the bears their valuation case.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in KLA Corp?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up KLA Corp, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track KLA Corp alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze KLA Corp on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

SpaceX (SPCX) Stock: Timing Your Entry Around Earnings and Lockup Expiration

Indonesian Rupiah: BI Tightening Expected to Buffer IDR Against US Dollar Strength, Says MUFG

DeFi TVL has been on a steady monthly decline since January