DraftKings: Risk-Reward Remains Attractive for Patient Investors

The post DraftKings: Risk-Reward Remains Attractive for Patient Investors appeared first on 24/7 Wall St..

Our DraftKings (NASDAQ:DKNG) price prediction lands within striking distance of where the stock trades today. After a brutal twelve months for shareholders, the question is whether the prediction markets pivot and Sportsbook margin expansion can outrun the litigation overhang and softer engagement metrics. My read: the risk/reward is balanced, with a slight tilt toward patient accumulation.

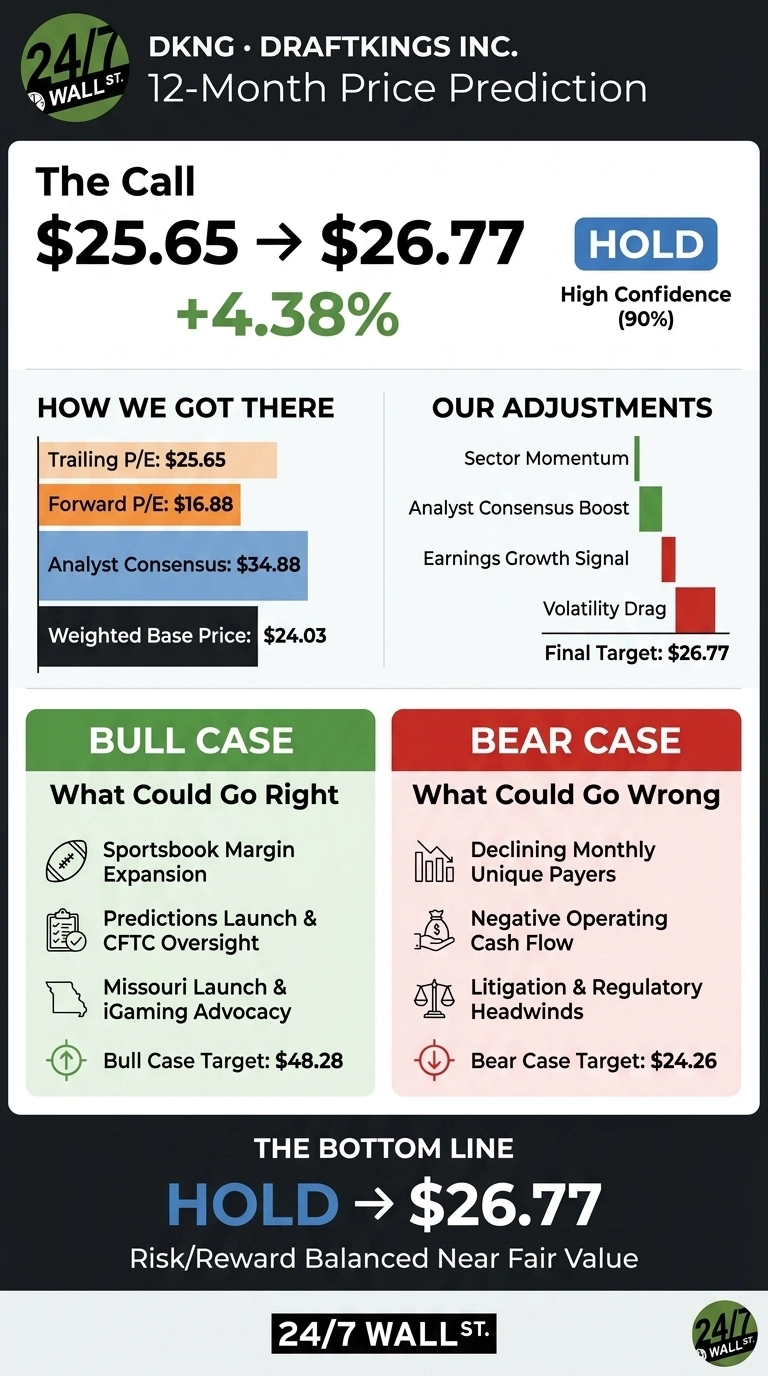

The 24/7 Wall St. price target for DraftKings is $26.77 over the next 12 months, implying 4.38% upside from $25.65. Our recommendation is hold, with a confidence level of 90%.

24/7 Wall St.

24/7 Wall St.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $25.65 |

| 24/7 Wall St. Price Target | $26.77 |

| Upside | 4.38% |

| Recommendation | HOLD |

| Confidence Level | 90% |

A Year of Pain, A Quarter of Hope

DKNG has fallen 36.68% over the past year and 25.57% year-to-date, with the stock sliding 10.91% in just the past week. Shares now sit 28% below their 52-week high of $48.78, though comfortably above the low of $20.46.

The Q1 2026 earnings report was a genuine bright spot. Revenue rose 8.83% to $1.65 billion, EPS of $0.20 beat by 16.41%, and Adjusted EBITDA jumped 64% to $167.85 million.

Still, the stock has been weighed down by a class action lawsuit filed April 29, 2026 alleging deceptive interface design, a Federal Reserve study linking sportsbook activity to consumer debt delinquency, and steady insider selling, including 62,500 shares from the Chief Legal Officer on June 11.

Why Bulls See a Breakout Ahead

The bull case rests on three pillars. First, Sportsbook net revenue margin expanded to 7.8% from 6.4%, with average revenue per Monthly Unique Payer up 21% to $131.

Second, the DraftKings Predictions launch under CFTC oversight, paired with the Crypto.com Derivatives partnership, opens a federally regulated event-contract market that could lift the entire valuation framework.

Third, the Missouri mobile launch and iGaming advocacy spend offer state-level optionality.

Morningstar has reiterated bullish commentary on the prediction-market expansion, and the consensus analyst target of $34.88 implies meaningful upside if execution holds. Our internal bull-case path projects DKNG reaching $48.28 within twelve months, a 88.23% total return.

The Risks Worth Watching

Bears point to a 4% YoY decline in Monthly Unique Payers to 4.2 million, negative Q1 operating cash flow of $48.4 million, and stock-based compensation of $65.2 million. State tax hikes in New Jersey, Louisiana, and Illinois compress structural margins.

To be fair, the cash-flow softness reflects $26.4 million in legalization advocacy and aggressive Predictions investment, both of which management frames as growth capex rather than recurring drag.

Litigation is the bigger swing factor. The PHAI product-liability suit and a Fed paper tying betting to delinquencies could pressure multiple expansion. Average analyst targets have already drifted from $44.58 to $38.80. Our bear-case scenario lands at $24.26 over twelve months.

DraftKings Price Prediction 2026-2030

The 24/7 Wall St. price target of $26.77 sits just above the current quote, and our hold rating carries 90% confidence. The constructive scenario hinges on MUP stabilization in Q2 and meaningful Predictions volume by year-end.

The cautious scenario is one where litigation expands or state tax increases spread further. The setup is balanced, and patience is the right posture.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $26.77 |

| 2027 | $27.08 |

| 2028 | $27.21 |

| 2029 | $29.53 |

| 2030 | $31.70 |

These projections assume DraftKings continues scaling Sportsbook margins and successfully establishes a defensible Predictions footprint. Significant upside or downside could result from federal prediction-market rulings, state iGaming legalization waves, or escalating product-liability litigation.

Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and DraftKings didn’t make the cut. Grab the names FREE today.

The post DraftKings: Risk-Reward Remains Attractive for Patient Investors appeared first on 24/7 Wall St..

You May Also Like

Binance to Halt EU Services Next Week After MiCA License Setback

Euro Holds Above 1.1400 as Falling Oil and Weaker Dollar Provide Support

Critical threshold at $0.073 for Dogecoin! What are the key signals traders should watch?