Spotify vs Netflix: One Growth Stock Has an Edge

The post Spotify vs Netflix: One Growth Stock Has an Edge appeared first on 24/7 Wall St..

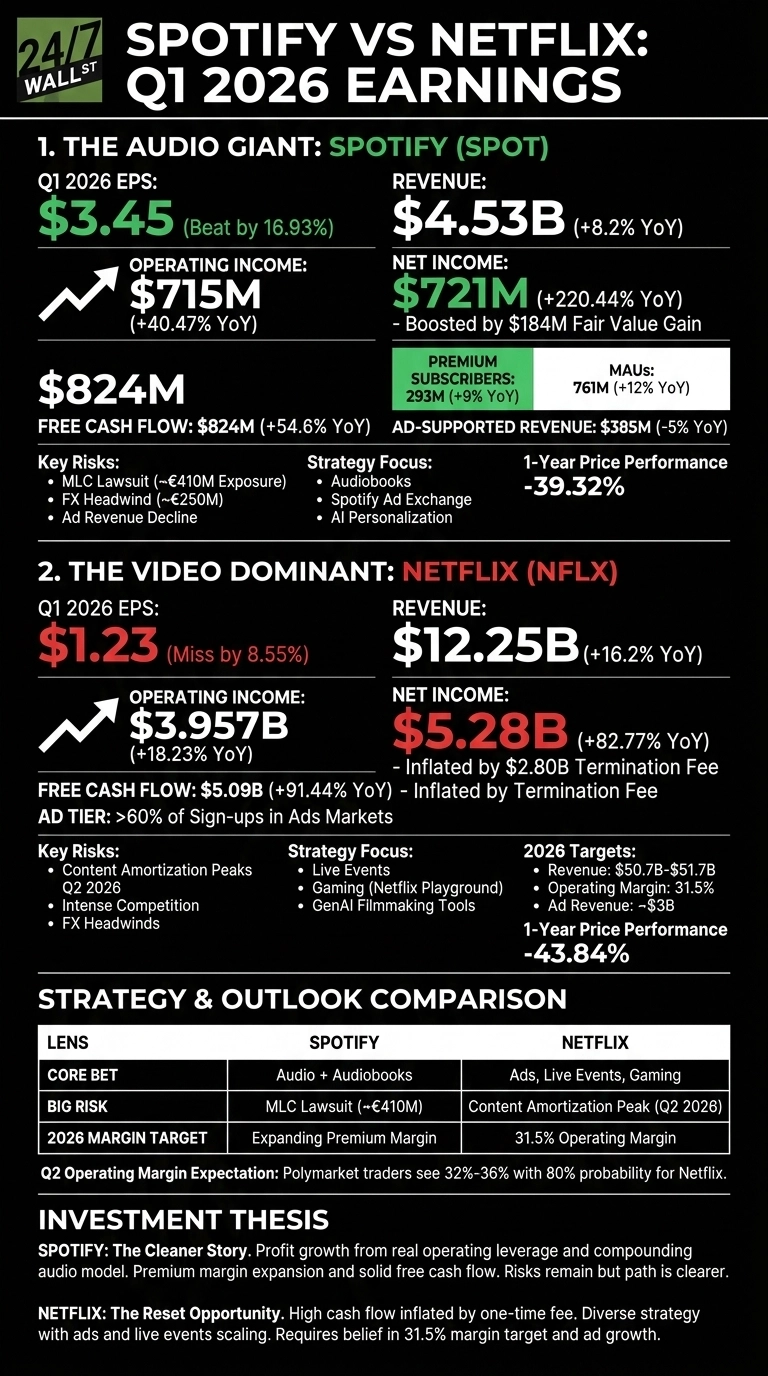

Spotify (NYSE:SPOT) and Netflix (NASDAQ:NFLX) both reported Q1 2026 earnings that sent each stock lower, but for very different reasons.

Spotify beat on profit and kept stacking subscribers. Netflix posted a headline-friendly cash flow number that was mostly a one-time check from a deal it walked away from. Two subscription giants. Two very different stories about where the money is actually coming from.

Audio Profits Land. A Termination Check Pads Video.

Spotify pulled $4.53 billion in revenue, up 8.19% year over year, with EPS of $3.45 against a $2.950 consensus. Premium subscribers reached 293 million, MAUs hit 761 million, and Premium gross margin expanded from 34% to 35%.

Price hikes added €0.42 to Premium ARPU. Ad-supported revenue fell 5%, and ad gross margin slipped to 13%. New features like SongDNA, Prompted Playlist, and a Spotify integration inside ChatGPT lean into personalization.

Netflix booked $12.25 billion in revenue, up 16.19%, but EPS of $1.23 missed the $1.345 consensus. The eye-popping $5.09 billion free cash flow was inflated by a $2.80 billion termination fee from the abandoned Warner Bros. deal. The ad tier was over 60% of sign-ups in ads markets, and advertiser count grew 70% to over 4,000 clients.

24/7 Wall St.

24/7 Wall St.

One Tightens Focus. One Widens the Net.

Spotify is doubling down on what it already owns: audio. The Partner Program courts video podcasters, audiobooks slot into Premium bundles, and the Spotify Ad Exchange leans into biddable inventory.

Netflix is sprinting in five directions at once: GenAI filmmaking tools from acquiring InterPositive, the Netflix Playground kids gaming app, video podcasts, live boxing, and the World Baseball Classic that became its most-watched program ever in Japan.

| Lens | Spotify | Netflix |

| Core Bet | Audio plus audiobooks | Ads, live events, gaming |

| Big Risk | MLC lawsuit, ~€410M exposure | Content amortization peaks in Q2 2026 |

| 2026 Margin Target | Expanding Premium margin | 31.5% operating margin |

The Next Test Is Ads Becoming Real Money

Netflix guided ad revenue to roughly $3 billion in 2026, double last year. Polymarket traders see Q2 operating margin landing between 32% and 36% with 80% combined probability.

Spotify’s path is narrower: keep nudging Premium ARPU higher without losing the price-sensitive cohort and stop the ad business from leaking. I’ll be watching whether Spotify’s biddable ad rollout halts that 5% ad revenue slide before it becomes a trend.

Both stocks have been punished. SPOT is down 39.32% over one year. NFLX is down 43.84%.

Why I Lean Spotify for the Cleaner Story

For my money, Spotify’s quarter was simply cleaner. Profit growth came from real operating leverage rather than a one-time deal-breakup check. Premium margin expansion and $824 million in free cash flow tell me the audio model is finally compounding. The 42 P/E asks a lot, and the MLC lawsuit could sting, so it isn’t risk-free.

Netflix fits a different investor. If you believe ads scale toward $3 billion, live sports keep printing sign-up records, and the 31.5% margin target holds, the post-earnings drawdown reflects a meaningful reset.

A couple of clean quarters without one-time inflation would strengthen the thesis. Walking away from Warner Bros. was disciplined, but it leaves the content engine relying on its own slate at exactly the moment competition from YouTube and TikTok keeps thickening.

Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and Netflix didn’t make the cut. Grab the names FREE today.

The post Spotify vs Netflix: One Growth Stock Has an Edge appeared first on 24/7 Wall St..

You May Also Like

Monday Market Wrap: Comcast Breakup, Alphabet’s Dow Debut, and Tech Stock Rally

Columnist cracks the 'unifying theory' behind Trump's seemingly manic behavior: opinion