Delta Stock Just Got a Wave of Target Hikes and a Downgrade in the Same Week. Here’s Where the Stock Could Go

Key Stats for Delta Stock

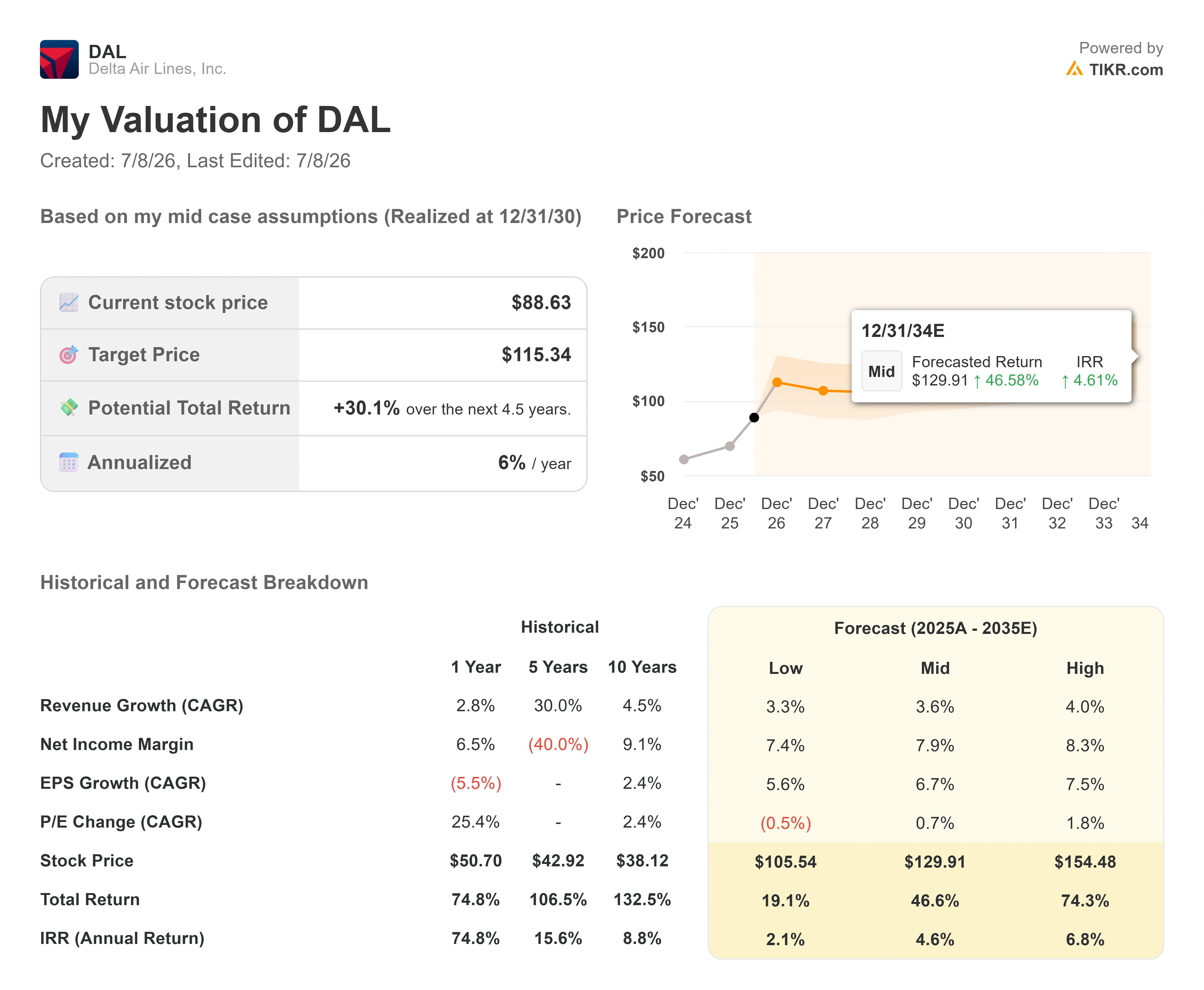

- Current Price: $88.63

- Target Price (Mid): ~$115

- Street Target: ~$96

- Potential Total Return: ~30%

- Annualized IRR: ~6% / year

- Max Drawdown: -23.11% (March 12, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Delta Air Lines (DAL) enters its Q2 print with Wall Street sending two signals at once, and they point in opposite directions. In early July, several banks lifted their price targets on Delta stock. Goldman Sachs moved to $116, Morgan Stanley to $115, Susquehanna to $108, and TD Cowen to $106. Then Raymond James downgraded the stock from Strong Buy to Outperform, even as it raised its own target to $104 from $80.

That is the tension worth sitting with. The target hikes say the ceiling is higher. The downgrade says the near-term upside is thinner. Delta stock has climbed roughly 83% over the past year and trades within about 7% of its record high, so the disagreement is not about whether the business is good. It is about whether the price already reflects how good.

Bulls point to a premium-heavy revenue base that keeps earning through a fuel shock. Bears point to a stock that has run hard and now needs a clean quarter to justify the move. The market cannot yet answer which side is right, and Q2 earnings on July 10 is where the answer starts to arrive.

Why the downgrade is not a bear call

The Raymond James move is easy to misread. Analyst Savanthi Syth cut the rating but raised the target, which is not the shape of a bearish call. Syth called Delta a top pick for long-term investors, citing structural advantages over network peers, a strong balance sheet, and a recent 15% dividend increase. The downgrade rested on one thing: the recent run-up in shares narrowed the gap between price and perceived fair value, thinning near-term upside. In plain terms, the company is still strong, but the stock caught up to it.

That reading matches the raw setup. The stock trades at $88.63, below the Street’s mean target of roughly $96 by only a modest margin, and above several individual targets entirely. When a name runs 83% in a year, the debate stops being about quality and starts being about entry price. This is the same question the target hikes are quietly answering in reverse: the banks raising numbers are betting Q2 pushes fair value higher, fast enough to keep the stock’s momentum intact.

Delta Street Targets (TIKR)

Delta Street Targets (TIKR)

See historical and forward estimates for Delta stock (It’s free!) >>>

The part of Delta that does not care what oil costs

The reason Delta commands this debate at all is a revenue base that has partly detached from the ticket. Premium seating, loyalty, cargo, and maintenance work behave differently from a coach fare when fuel spikes, and management is building the highest margin of those streams into a data business.

The clearest example is connectivity. At TD Cowen’s consumer conference on June 3, Chief Marketing and Product Officer Ranjan Goswami detailed Delta Sync, the airline’s logged-in onboard platform. Goswami said 30% of customers who log into Delta Sync WiFi stay inside Delta’s own environment rather than leaving for the open internet, and seatback screen login rates using a birthday now exceed 40%. Those are identity-authenticated channels Delta can sell against, the same logic that makes a social feed valuable.

The forward version of that runs on satellite. Delta’s Amazon Leo agreement covers an initial 500 aircraft starting in 2028, delivering 1 gigabit per second on the downlink and 400 megabits on the uplink, faster than anything currently in service. Goswami’s framing matters because it explains why Delta chose Amazon over a pure connectivity vendor: Amazon is not only a pipe to the airplane but the largest consumer brand in the world, opening shopping, content, and gaming use cases onboard. That is a revenue line that scales with engagement, not with jet fuel.

The valuation question the run created

Here is where the story gets harder. Delta trades at roughly 14x forward earnings and 7.9x forward EV/EBITDA, which is not expensive for a business generating 25% return on equity and 12% return on invested capital. On quality metrics, Delta screens as a compounder that happens to be filed under airlines. The refinery it owns through Monroe Energy gives it a fuel hedge that no major peer carries, and net debt to EBITDA has fallen to 1.32x, a balance sheet that most of the sector cannot match.

The problem is not the multiple. It is the math after an 83% run. The stock already sits close to the Street’s average target, which means the market has pulled forward a chunk of the recovery that fuel relief and premium demand were supposed to deliver over the next year. Jet fuel has retreated from its wartime peak, but that relief is visible to everyone and tends to be priced quickly. According to the International Air Transport Association fuel monitor, the global average jet fuel price was about $117 per barrel as of July 1, down sharply from roughly $142 in June as Middle East supply fears eased. If Q2 margins disappoint, a stock trading near consensus has little cushion. If they beat, the target hikes look prescient, and the downgrade looks early. The setup rewards the quarter, not the memory of the rally.

Against peers, Delta’s premium is defensible on structure: it is the only major U.S. carrier that owns a refinery, giving it a fuel hedge no rival holds, and it carries an investment-grade balance sheet most of the sector cannot match. That justifies a premium to a commodity carrier. Whether it justifies a premium to Delta’s own recent price is the open question, and it is the one Raymond James flagged.

Delta NTM EV/EBITDA (TIKR)

Delta NTM EV/EBITDA (TIKR)

See how Delta performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $88.63

- Target Price (Mid): ~$115

- Potential Total Return: ~30%

- Annualized IRR: ~6% / year

Delta Advanced Valuation Model (TIKR)

Delta Advanced Valuation Model (TIKR)

See analysts’ growth forecasts and price targets for Delta stock (It’s free!) >>>

The TIKR mid-case values Delta stock at about $115 by the end of the model horizon, an approximately 30% total return, or around 6% annualized. That is a positive setup, but a modest one, and it captures why the stock can be both high quality and fully priced at once. The model’s own annualized return sits below Delta’s stronger historical rate, reflecting a market that has already absorbed much of the near-term recovery.

Two revenue drivers anchor the case. The first is premium and loyalty mix, which holds the revenue CAGR near 4% even when main-cabin demand softens. The second is international network capacity across the Atlantic and Pacific, where Delta has built leadership positions. The margin driver is net income margin holding near 8%, supported by the refinery hedge and disciplined capacity. The primary risk is fuel: if elevated jet fuel persists into the back half of 2026, the margin expansion the rally is pricing gets pushed out, and a stock already near the Street target has little room to absorb the miss.

The upside case is a clean Q2 beat that lifts full-year guidance and pulls the mean target toward the high end near $115. The downside case is a fuel-driven margin miss that leaves a richly priced stock searching for support.

Conclusion

The one number that settles this debate arrives July 10, before the open: Q2 operating margin, and the full-year guidance that comes with it. Consensus expects EPS around $1.45 on revenue of roughly $17.7 billion to $18.8 billion. Good looks like an in-line or better margin plus a raised full-year outlook, which validates the target hikes and makes the Raymond James downgrade look premature. Bad looks like fuel eating the premium-demand story, which hands the near-term skeptics a richly priced stock with no cushion. Delta has beaten EPS estimates in each of the last four quarters, so the bar is not whether it beats. The bar is whether the guide is strong enough to justify a stock that has already run to the edge of the Street’s targets.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Delta?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Delta, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Delta alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Delta on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

Bitcoin & Ethereum Inflows Hit 1-Year Low as Crypto Investors Brace for Fed Decision – BTC Eyes $120K

Critical USDT0 Response to Drift Hack Exposes Stark Contrast in Stablecoin Security Protocols

Metaplanet Stock Passes MARA to Become Third-Largest BTC Holder — Stock Slips Anyway