MARA Holdings Is Betting Its Future on Power, Not Bitcoin

Key Stats for MARA Stock

- 52-Week Range: $6.66 to $23.45

- Current Price: $14.54

- Street Mean Target: $18.16

- Market Cap: ~$5.5B

- LTM Gross Margin: 45.3%

- Energized Hashrate: 72.2 EH/s

- BTC Holdings: 35,303 BTC (~$2.4B)

- 5-Year Beta: 5.43

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

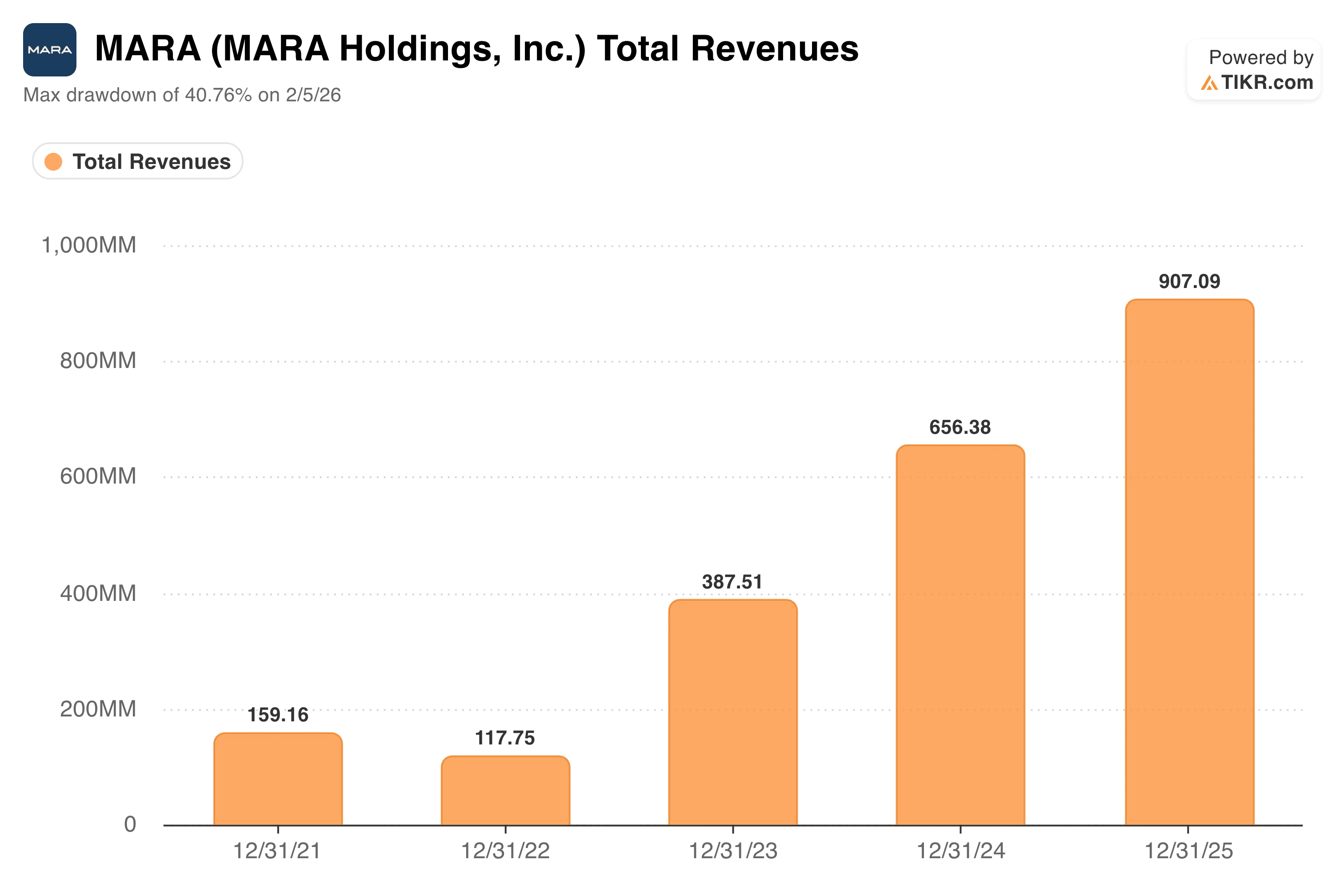

Revenue Doubled in 2 Years. Bitcoin Drove Almost All of It.

MARA’s (MARA) revenue trajectory looks impressive on the surface. Annual revenue grew from $118 million in 2022 to $907 million in 2025, a nearly eightfold increase in three years. But the driver of that growth is not operational leverage or market share gains in the traditional sense. It is almost entirely the price of Bitcoin.

MARA Total Revenues. (TIKR)

MARA Total Revenues. (TIKR)

MARA mines Bitcoin, holds it on its balance sheet, and recognizes revenue based on the coins it produces and the price at which they are valued. When Bitcoin was in the depths of its 2022 bear market, revenue collapsed to $118 million.

When Bitcoin climbed back above $100,000 in late 2024 and through 2025, revenue followed. Q1 2026 illustrated the inverse just as clearly: revenue fell 18% to $174.6 million as Bitcoin’s average price declined roughly 18% over the same period.

That relationship is the central tension in the MARA investment thesis. The business is operationally improving. Energized hashrate grew 33% year over year to 72.2 exahashes per second in Q1 2026, cost per petahash per day improved 3%, and purchased energy cost per kWh held at $0.04 for owned sites.

MARA is genuinely getting more efficient at mining. But no amount of operational improvement changes the fact that quarterly results will be driven by where Bitcoin trades, not by anything management controls.

Chairman and CEO Fred Thiel acknowledged this directly in the Q1 shareholder letter, framing the pivot in plain terms: “The next phase of digital infrastructure value creation will be shaped by control of power.”

See analysts’ growth forecasts and price targets for MARA Holdings stock (It’s free!) >>>

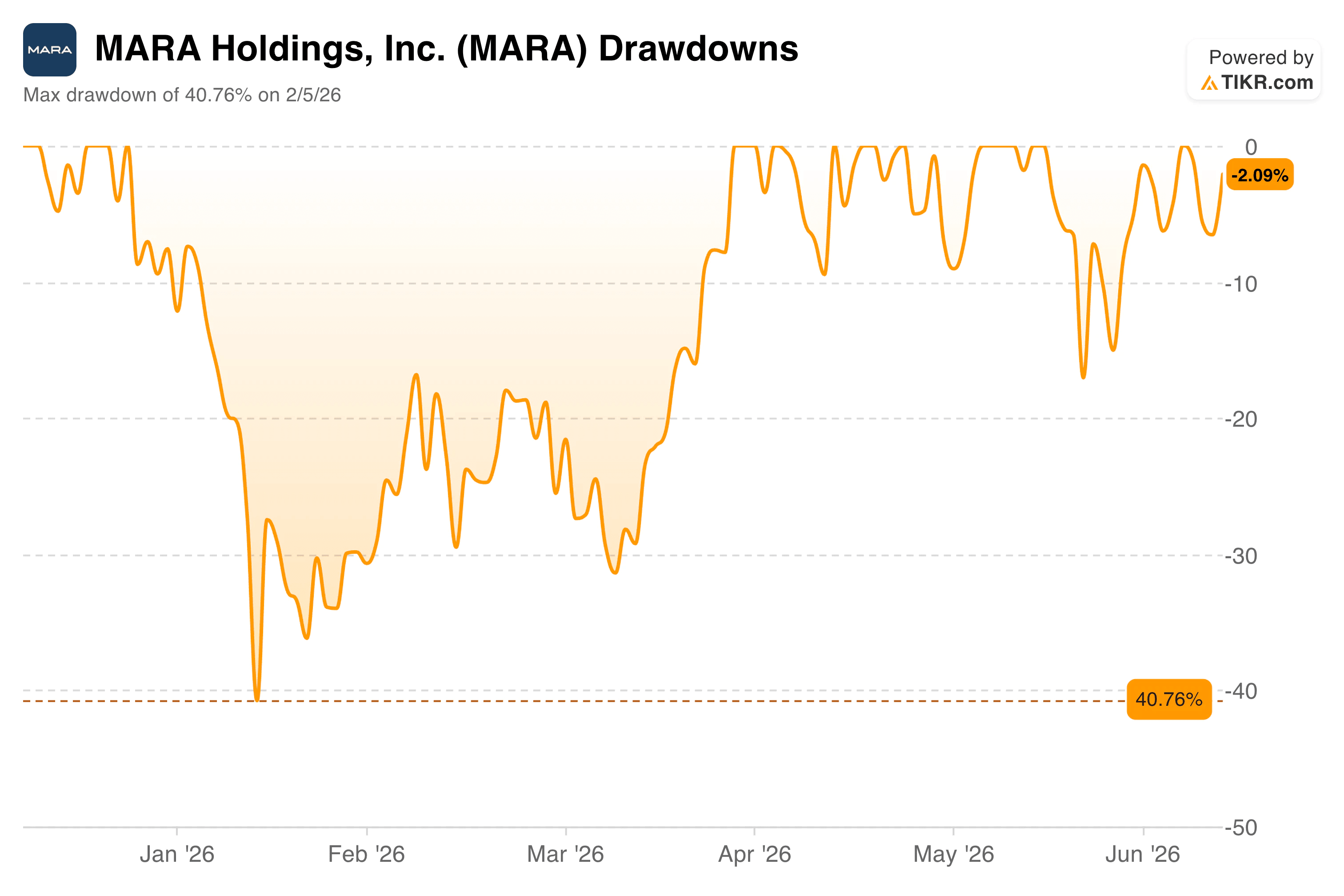

A 41% Drawdown in 6 Weeks. Then a Full Recovery.

MARA’s 5-year beta of 5.43 is among the highest for any publicly traded stock. What that number means in practice is visible in the drawdown chart.

The stock fell as much as 41% from its peak in early January to its trough on February 5, then recovered almost entirely by late April as Bitcoin stabilized and the strategic narrative around Long Ridge and the Starwood joint venture began drawing investor interest.

MARA Holdings Drawdowns. (TIKR)

MARA Holdings Drawdowns. (TIKR)

That kind of volatility is not incidental to the thesis. It is the thesis, for better or worse. Investors in MARA are implicitly making a call on Bitcoin’s direction, on management’s ability to execute the infrastructure pivot, and on the market’s willingness to eventually value MARA as something other than a leveraged Bitcoin proxy. All three of those bets need to go right simultaneously for the stock to work over a multi-year horizon.

The strategic moves management made in Q1 are genuinely significant. MARA announced a definitive agreement to acquire Long Ridge Energy and Power, a 505 MW combined-cycle gas turbine plant sitting on 1,600 contiguous acres in the PJM Interconnection, one of the most active power markets in North America.

The plant already generates contracted cash flow, operates at under $0.015 per kWh all-in, and wraps around MARA’s existing Bitcoin mining operations at Hannibal. Management intends to use the site as the foundation for a premier AI data center campus, with over 1 GW of total potential capacity.

The Starwood joint venture, announced in Q1 and now advancing to active site preparation, gives MARA a capital-efficient path to convert its power assets into ownership of AI infrastructure without bearing the full construction cost.

Approximately 90% of MARA’s non-hosted capacity is currently being considered for conversion to digital infrastructure.

Read the full MARA Holdings Transcript on TIKR to see the 2026 guidance breakdown >>>

What the Street Says About MARA

Without a traditional valuation model, analyst targets provide the clearest forward-looking anchor. The street mean target currently stands at $18.16 against a current price of $14.54, implying about 25% upside.

The range is wide: the high target is $30, and the low is $7, a spread that reflects genuine disagreement about how to value a company mid-transition.

MARA Street Targets. (TIKR)

MARA Street Targets. (TIKR)

The analyst community has eight buy or outperform ratings, five holds, and one sell. That distribution is modestly constructive but not particularly convincing.

Notably, the mean target was around $23 in September 2025 before declining sharply as Bitcoin fell, illustrating how closely analyst price targets track Bitcoin sentiment rather than any assessment of MARA’s infrastructure progress.

As Long Ridge closes and tenant leasing shifts from pipeline to signed contracts, the infrastructure narrative may carry more weight in how analysts frame their targets.

Should You Invest in MARA Holdings, Inc.?

MARA is two companies in transition: a Bitcoin miner whose results will continue to swing with BTC prices, and an emerging digital infrastructure platform whose value has not yet been contracted or proven.

The Long Ridge acquisition and Starwood JV are compelling strategic moves, but they are pre-revenue and pre-tenant.

Investors who are bullish on Bitcoin and patient about the infrastructure buildout have a real case here. Everyone else faces a stock with a beta above 5 and no traditional earnings anchor to lean on.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

What Happens to the XRP Price if the Crypto Bear Market Gets Worse?

The Manchester City Donnarumma Doubters Have Missed Something Huge

Solana SOL Reclaims $72, But Fading On-Chain Metrics Signal Weakening DEX Momentum